Solid first half; Industry searching for new equilibrium

SBM Offshore is happy to report better than expected revenue. The Company continues to see a healthy appetite for itsprojects, as evidenced by the 45% taken up by joint venture partners in the Turritella project as well as the recentlyannounced US$1.55 billion of project financing for Cidade de Saquarema. Progress in discussions with Brazilianauthorities continues via the announced signing of a Memorandum of Understanding. SBM Offshore continued to achieveover 99% uptime across the fleet while Directional¹ Backlog ended the period at US$20.0 billion. Full year Directional¹ revenue guidance has been increased to at least US$2.6 billion.Bruno Chabas, CEO of SBM Offshore, commented:

“The current downturn is having a profound impact on our industry, which is faced with the challenge to reinvent itself to survive profitably in the current oil price environment. SBM Offshore is determined and confident it can play its part basedon its track record of technological innovation, its willingness to take decisive action through its restructuring and backedby its strong lease and operate cash flow.”

Financial Highlights

- Directional¹ revenue ahead of expectations at US$1.6 billion

- Underlying Directional¹ EBIT of US$255 million and underlying EPS of $0.78 per share

- Directional¹ Backlog stood at US$20.0 billion

- Cash and undrawn committed credit facilities at the end of the period stood at US$1,364 million

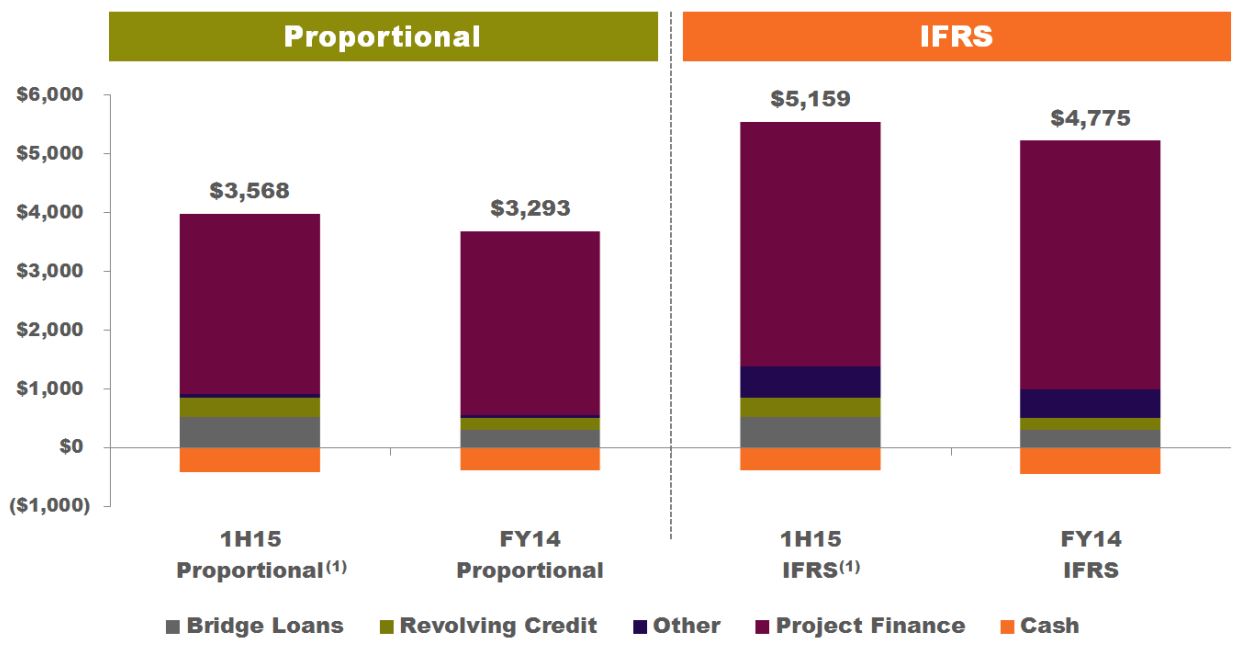

- Proportional net debt at the end of June stood at US$3,568 million

- Joint Venture partner participation in the Turritella project totaling 45%

- Memorandum of Understanding signed with Brazilian authorities

- Project financing secured post period for FPSO Cidade de Saquarema totaling US$1.55 billion

Guidance

The Company is updating 2015 Directional¹ revenue guidance from at least US$2.2 billion to at least US$2.6 billion. Theincrease is primarily attributable to the announced 45% stake in the Turritella project taken up by joint venture partners.Turnkey revenue guidance for 2015 is now expected to be US$1.4 billion versus US$1.0 billion previously, while Lease &Operate segment guidance of US$1.2 billion remains unchanged. Proportional net debt guidance below US$3.5 billion isbeing confidently reiterated for FY2015.

Management is introducing Directional¹ capital expenditure guidance. For the remaining three finance lease vesselsunder construction Directional¹ capital expenditure is expected to total approximately US$265 million, with approximately75% falling in the second half of 2015. Directional¹ capital expenditure excludes changes in net working capital and ispresented net of upfront payments for FPSOs Cidade de Maricá and Cidade de Saquarema.

FIRST HALF 2015 RESULTS

Project Review

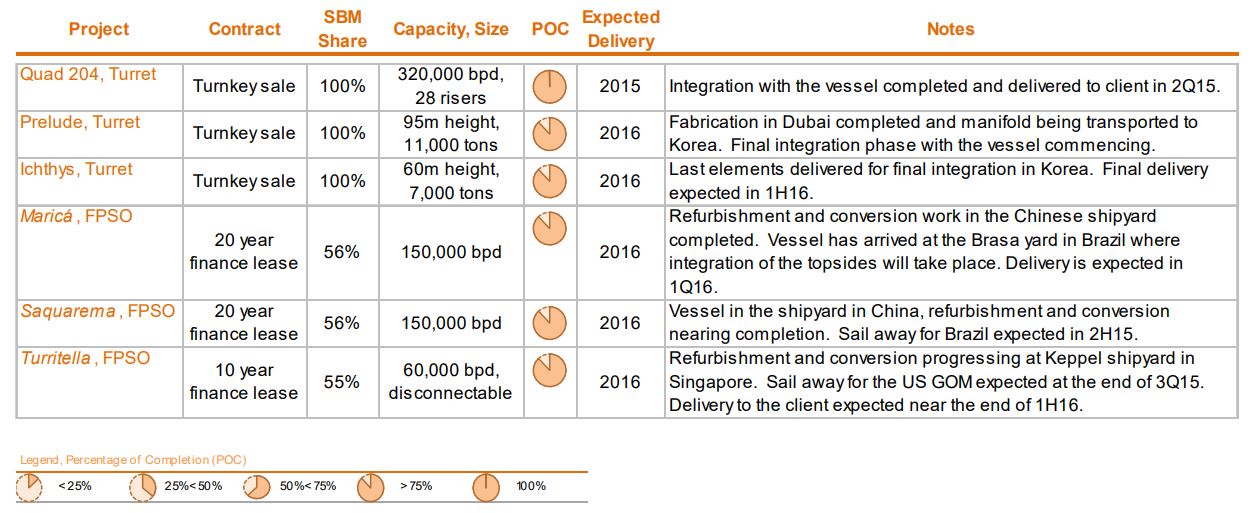

FPSO Cidade de Maricá and Cidade de Saquarema (Brazil)

Construction is ongoing for the two finance leased vessels. Cidade de Maricá berthed safely at the Brasa yard near Riode Janeiro on July 9, 2015 where topside integration work is ongoing in order to meet local content requirements. Deliveryto the client is expected in 1Q16.

Concurrently refurbishment and conversion work on Cidade de Saquarema progressed during the first half of 2015 at aChinese yard and is nearing completion. Sail away for Brazil, where integration of the topside will take place, is expectedin the second half of 2015.

The charter contract for both vessels includes an initial period of 20 years with extension options. The client will makeupfront payments at first oil totalling US$282 million, split between both vessels, of which US$158 million represents SBMOffshore’s 56% share in the joint ventures. The two double-hull sister vessels will be moored in approximately 2,300meters of water depth and possess a storage capacity of 1.6 million barrels each. The topside facilities of each FPSOweigh approximately 22,000 tons, will be able to produce 150,000 bpd of well fluids, have associated gas treatmentcapacity of 6,000,000 Sm3/d and water injection capacity will be 200,000 bpd each.

FPSO Turritella (US Gulf of Mexico)

Construction continued for the finance leased vessel in the first half of the year, with refurbishment and conversion worknear completion at Keppel Singapore. Sail away for the Gulf of Mexico, where anchoring and commissioning will takeplace, is expected during the second half of 2015 with delivery to the client expected near the end of 1H16. The chartercontract includes an initial period of 10 years with extension options up to a total of 20 additional years.

When installed at almost three kilometers of water depth, the FPSO Turritella will be the deepest offshore productionfacility of any type in the world. The vessel is a typical Generation 2 design, with a disconnectable internal turret andprocessing facility capacity of 60,000 barrels of oil per day (bpd) and 15 mmscfd of gas treatment and export.

N’Goma FPSO (Angola)

Formal Production Readiness Notice was received in early January 2015 going into effect retroactively to late November.The vessel is producing and has been on-hire generating dayrate retroactively since November 28, 2014.

FSO Yetagun (Myanmar)

Following fifteen years of operation with no lost time incident, the client has notified the Company of its intention toexercise an additional three-year extension option. Additionally, a brownfield life extension award totalling approximatelyUS$30 million has been agreed upon. The Yetagun Life Extension project is expected to take 18 months and becompleted in July 2016. The vessel will remain in normal operation while brownfield life extension work is beingcompleted.

FPSO Marlim Sul (Brazil)

Previously announced decommissioning activities, that were expected to be completed during the second quarter of 2015,have ceased as the client reviews continued production alternatives for the Marlim Sul field. The vessel is receiving astandby dayrate through the end of 2015 while awaiting client confirmation to complete decommissioning activities.

Turret Mooring Systems

The three large, complex turrets for Prelude FLNG, Quad 204 and Ichthys are progressing in accordance to clients’schedule. Integration of the Quad 204 turret with the vessel has been completed in Korea and the client has accepteddelivery, while fabrication work on Prelude FLNG has been completed in Dubai with final integration in Korea. The lastelements of the Ichthys turret have been delivered for final integration in Korea with expected delivery in early 2016.

Main Projects Overview

Directional¹ capital expenditure through the first half of 2015 amounted to a combined total of US$265 million, reflectingthe advanced construction progress of the Company’s main projects which are expected to be completed over the nexttwelve months. These amounts correspond to the SBM Offshore share in SBM Inc. (the Company’s constructionsubsidiary) costs as well as costs directly incurred at the joint venture level.

HSSE

The Company has continued to achieve improved safety performance in the first half of 2015 with the lowest frequenciesof recordable injuries and lost time injuries since 2007. Total Recordable Injury Frequency Rate (TRIFR) improved 30% to0.15 compared to 0.22 at the end of 2014, while the Lost Time Injury Frequency Rate (LTIFR) improved by 80% to 0.01 inthe first half of 2015 from 0.05 at the end of 2014.

Furthermore, the focus on the potentially severe incidents and on process safety has been strong allowing the Companyto reach the lowest level frequency rate since 2011. The volume of gas flared was 25% better than target, however GHGemissions per unit of production was 25% above the industry benchmark for first half year. Offshore energy consumptionand oil discharged from produced water improved compared to last year and stood well above the industry benchmark.

Compliance

On March 16, 2015 SBM Offshore announced the signing of a Memorandum of Understanding (MoU) with the BrazilianComptroller General’s Office (Controladoria-Geral da União – “CGU”) and the Attorney General’s Office (Advocacia Geralda União – “AGU”). This MoU sets a framework between the Company, the CGU and the AGU for discussions on apotential mutually acceptable settlement and for the disclosure by SBM Offshore of information relevant to the CGU’sinvestigations.

The Company continues to cooperate with all requests for information and is in active dialogue with the BrazilianComptroller General’s Office in order to come to an agreement to close the matter in Brazil.

Turritella Joint Venture

Effective June 30, SBM Offshore completed the divestment of a 45% stake in the Turritella project to joint venture partnersMitsubishi Corporation (MC) and Nippon Yusen Kabushiki Kaisha (NYK Line). Subsequently, the Company cash calledthe joint venture partners for their share in the construction costs, and an amount of US$446 million was received on July15, 2015. The total partners’ cash contribution to the Turritella project is expected to amount to approximately US$590million. Future milestone payments will follow the stages of completion of the project.

Post-Period Events

Cidade de Saquarema Project Financing

On July 27, 2015 the Company secured project financing for FPSO Cidade de Saquarema totalling US$1.55 billion, at aweighted average cost of debt of 5.1%, from a consortium of sixteen international banks with insurance cover from fourExport Credit Agencies (ECA). The financing consists of three tranches, two with ECA insurance cover and onecommercial, with fourteen year post-completion maturities. This is the largest project financing in the Company’s history.

Directional¹ Backlog

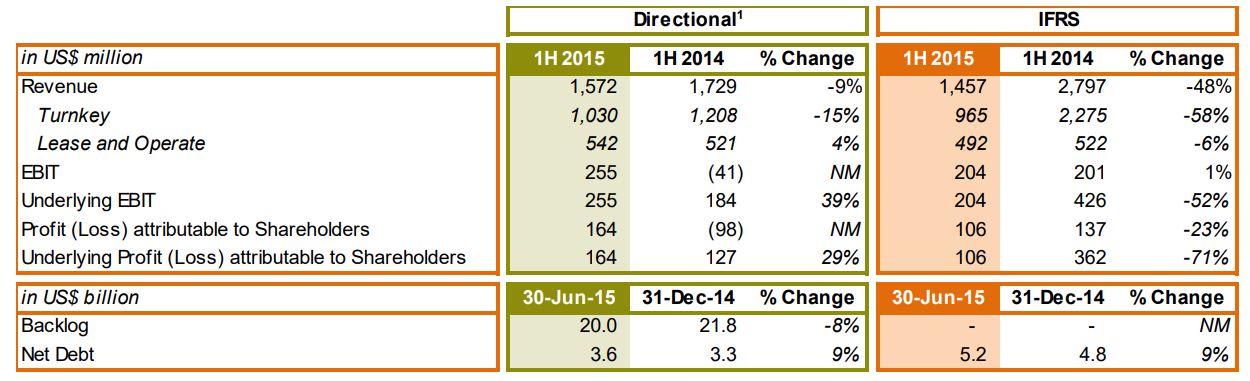

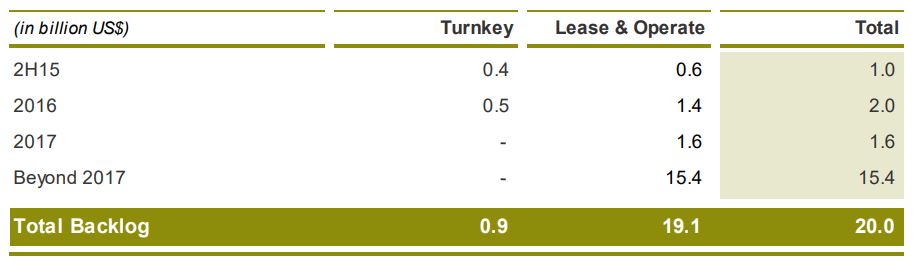

Directional¹ backlog at the end of June 2015 came in at US$20.0 billion compared to US$21.8 billion at the end of 2014.This reduction reflects the low order intake of US$0.3 billion, the revenue generated during the first half of 2015 and theUS$0.5 billion decrease related to the 45% stake in the Turritella project by joint venture partners. Approximately 37% oftotal future bareboat revenues will be generated from the lease contracts which have yet to commence operations. Thoseinclude FPSOs Cidade de Maricá, Cidade de Saquarema and Turritella.

Directional¹ Turnkey backlog decreased to US$0.9 billion compared to US$1.1 billion at the end of 2014 due to theexecution of projects under construction, while being partially offset by the 45% partner’s stake in the Turritella project.Backlog as of June 30, 2015 is expected to be executed as per the below table:

Order Intake

New orders signed during the first half of 2015 totalled US$161 million, and variation orders totalled US$111 million. Themain new orders signed during the period include the Yetagun brownfield life extension award and various offshorecontracting awards.

Restructuring

As announced with the first quarter 2015 trading update on May 7, workforce reductions over the period 2014 and 2015were revised from 1,200 to 1,500 positions as a result of a further review of the cost structure and a prolonged marketdownturn.

Upon announcement of the original restructuring on December 11, 2014 the Company stated that annualized savings ofapproximately US$40 million related to Company employees were expected. Management also indicated that redundancycosts were likely to total approximately US$25 million, of which US$8 million were taken in 2014 and a further US$17million would be incurred in 2015.

Updated 2015 cost provisions of approximately US$49 million, an increase of US$32 million versus previous expectations,have been taken in the first half results and the Company anticipates realizing annualized savings of approximately US$80million compared to previous guidance of US$40 million.

The Company’s adaptation to market developments is focused on retaining core competencies. While expectations fororder intake remain subdued, maintaining some engineering overcapacity remains crucial to being properly positioned fora market upturn.

Divestment Update

The Company completed the disposal of FPSO Brasil, Kuito and VLCC Alba in the first quarter of 2015.

Master Limited Partnership

Following the completion of a strategic review of alternatives, the Company announced on November 13, 2014 its intent topursue the development of a master limited partnership (MLP). Structuring work is progressing with the Company workingtowards receiving the required regulatory approvals and filing a registration statement with the Securities and Exchange

Commission. The Company currently expects any initial public offering of common units in the MLP to occur during thesecond or third quarter of 2016. This is revised from initial expectations of third quarter 2015. The anticipated offeringwould be subject to market conditions.

Extraordinary General Meeting of Shareholders

The Company will hold an Extraordinary General Meeting of Shareholders on November 4, 2015 where it will be proposedthat Bruno Chabas (CEO) be reappointed as a member of the Management Board and CEO effective January 1, 2016 fora second four year term in office.

Investing in Our Future

The Company announced in 2014 a focused investment program in Research and Development (R&D), projectcapabilities (Odyssey24) and increased fleet maintenance, which would total approximately 2.5%-3% per year for twoyears of 2014 Directional¹ revenue guidance of US$3.3 billion.

The R&D and Odyssey24 programs are on track with first half 2015 spending amounting to US$41 million compared toUS$28 million in the year-ago period. R&D efforts are largely focused on the new reality of delivering complex deepwaterprojects in the current oil price environment, while Odyssey24 is focused on step changes in project and supply chainmanagement with an expected payback on investment with the next Generation 3 FPSO project.

The Odyssey24 project will be completed in the second half of 2015, while the increased Research and Developmentefforts continue. A substantial part of the efforts represent internal workforce, making optimal use and retaining availableengineering capacity during the current downturn.

Outlook and Guidance 2015

The market outlook remains challenging as the Company continues to see delays in final investment decisions, andultimately awards, by clients. The Company maintains its positive medium to long-term outlook as the Company considersdeepwater development a secular growth story.

The Company is updating 2015 Directional¹ revenue guidance from at least US$2.2 billion to at least US$2.6 billion. Theincrease is primarily attributable to the announced divestment of a 45% stake in the Turritella project. Turnkey revenueguidance for 2015 is now expected to be US$1.4 billion versus US$1.0 billion previously, and Lease & Operate segmentguidance of US$1.2 billion remains unchanged. Proportional net debt guidance below US$3.5 billion is confidentlyreiterated for FY2015.

Management is introducing Directional¹ capital expenditure guidance. For the remaining three finance lease vesselsunder construction Directional¹ capital expenditure is expected to total approximately US$265 million, with approximately75% falling in the second half of 2015. Directional¹ capital expenditure excludes changes in net working capital and ispresented net of upfront payments for FPSOs Cidade de Maricá and Cidade de Saquarema.

FINANCIAL REVIEW

Directional¹ Performance

In 2013, SBM Offshore decided to extend its reporting with non-IFRS disclosures showing audited disclosures of Backlogand Income Statement based on Directional¹ principles. Directional¹ reporting principles stand as follows:

- Directional¹ reporting represents an additional non-GAAP disclosure to IFRS reporting

- Directional¹ reporting assumes all lease contracts are classified as operating leases

- Directional¹ reporting assumes all JVs related to lease contracts are consolidated on a proportional basis

- All other accounting principles remain unchanged compared to applicable IFRS standards.

Directional¹ revenue for the first half of 2015 was down by 9% year-over-year to US$1,572 million versus US$1,729 millionin the first half of 2014, reflecting the slowdown of Turnkey activity as a result of oil and gas macro market conditions.Directional¹ revenue by segment was as follows:

- Directional¹ Turnkey revenue decreased by 15% from the year-ago period reflecting lower activity on theconstruction of FPSOs Cidade de Maricá and Saquarema during the first half of 2015, the lack of significantorder intake, partially offset by additional revenue invoiced to the new partners in the Turritella joint venturecompany.

- Directional¹ Lease and Operate revenue increased by 4% versus the first half of 2014 mainly due to thecommencement of production of FPSOs Cidade de Ilhabela and N’Goma FPSO in late 2014 offset byFPSOs Brasil, Kuito and Marlim Sul no longer being in production in 2015.

Directional¹ Earnings Before Interest and Taxes (EBIT) for the first half of 2015 increased to US$255 million comparedwith a loss of US$41 million in the year-ago period, which featured a US$240 million provision for the settlement of theinvestigation of improper sales practices and the US$15 million release of an impairment related to Deep Panuke.Adjusted for both exceptional items in 2014, EBIT increased by 39% from US$184 million to US$255 million in the first halfof 2015. This was primarily attributable to:

- Directional¹ Turnkey EBIT increased by 60% due to the strong performance of various projects during theperiod and the positive contribution of the gross margin recognised during the engineering, procurement andconstruction of FPSO Turritella started in 2013 on the new partners who acquired a stake of 45% in thisproject.

- Directional¹ Lease and Operate EBIT increased by 7% compared with the year-ago period but includes theimpact of increased costs associated with the two year focused fleet maintenance programme. Directional¹ Lease & Operate EBIT Margin came in at 27.6% in the first half of 2015 including some restructuring costs,compared to the 26.7% during the first half of 2014.

- As a result of an on-going review of the cost structure and continued market downturn, the Company’sworkforce reduction is now expected to amount to at least 1,500 positions worldwide over the period 2014and 2015. Restructuring costs accounted for as “Other operating expense” over the period represent US$49million, of which US$32 million relate to the Turnkey segment, US$11 million for Lease and Operate, andUS$6 million for the “Other” segment.

Directional¹ Overhead expenses reported in the “Other” segment increased to US$61 million in the first half of 2015 fromUS$47 million in the year-ago period. The strong level of overhead expenses is mainly attributable to the ongoinginvestments in the two year transformation program, Odyssey 24, which will be completed by the end of 2015. In general,Overhead expenses reflect the additional efforts to maintain the Company’s leading technological position, as well as one-offitems such as expenses related to the investigation in Brazil.

For the first half of 2015, Directional¹ EBITDA increased to US$430 million, compared to US$98 million in 2014. Adjustedfor non-recurring items, Underlying Directional¹ EBITDA increased by 27% due to strong project execution positivelyimpacting the Turnkey segment and the positive effects of the partner contributions to the Turritella project.

Directional¹ net financing costs totalled US$70 million in the first half of 2015, up from US$47 million in the year-agoperiod. The increase was primarily due to interest costs related to the project financings of FPSOs Cidade de Ilhabela andN’Goma FPSO as both units commenced production at the end of 2014.

SBM Offshore recorded a Directional¹ net profit of US$164 million for the first half of 2015 or US$0.78 per share,compared with a US$98 million loss or US$0.47 per share for the first half of 2014. Adjusted for the US$240 millionprovision related to the settlement of the investigation of potentially improper sales practices and the US$15 millionrelease of an impairment related to Deep Panuke in 2014, underlying Directional¹ net income increased by 29% year-on-yearto US$164 million or US$0.78 per share, compared to US$127 million or US$0.61 in the first half of 2014 for thereasons stated above.

IFRS Performance

IFRS revenue for the first half of 2015 amounted to US$1,457 million, decreasing by 48% compared to US$2,797 million inthe year-ago period as a result of the reduction of investments in finance lease contracts under construction.

Under IFRS, the 45% stake taken by Joint Venture partners in the Turritella project has no visible impact. The Turritellalease is classified as a finance lease, implying the project is already accounted for as a 100% sale during constructionincluding deemed construction profit. Also of importance is that SBM Offshore will retain control of the companies owningand operating the FPSO, resulting in continued full consolidation as if no partner contribution had taken place except forthe recognition of additional non-controlling interests.

IFRS EBIT for the first half of 2015 remained stable to US$204 million compared to US$201 million in the year ago periodwhich was including the US$240 million provision in 2014 for the settlement of the investigation of potentially impropersales practices and the US$15 million impairment release on Deep Panuke. The underlying decrease of IFRS EBITreflects the reduction of investments in finance lease projects under construction, due to projects nearing completion in2015, and the lack of any impact under IFRS in the consolidated Income statement of the 45% partner’s share in the jointventure companies owning and operating FPSO Turritella, which remain both fully controlled under IFRS 10.

IFRS net income attributable to shareholders came in at US$106 million compared to US$137 million a year ago.

Statement of Financial Position

Total assets remained stable at US$11.3 billion as of June 30, 2015 compared to US$11.1 billion at year-end 2014. Thisreflects the lower investments in FPSOs Cidade de Maricá, Cidade de Saquarema and Turritella during the period and theplanned amortisation of property, plant, and equipment and finance lease receivables.

As of June 30, 2015 net debt under IFRS standards slightly increased to US$5,159 million reflecting lower investments inthe ongoing Lease & Operate projects under construction. Cash and cash equivalent balances came in at US$389 millionand committed, undrawn, long-term bank facilities stood at US$975 million. The average cost of debt is 4.2%, unchangedfrom the end of 2014.

Total equity as of June 30, 2015 slightly increased at US$3,363 million compared to December 31, 2014. The Company’snet debt to total equity remained stable at 152% at year-end 2014 to 153% at the end of the first half of 2015.

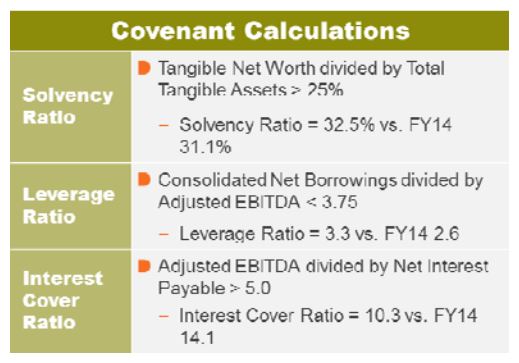

The Company’s solvency ratio stood at 32.5% while the leverage ratio came at 3.3 times and the interest cover ratio camein at 10.3 times, all firmly within covenant requirements.

Including cash outflows for finance leases under construction previously reported as investing activities, cash fromoperating activities was negative US$394 million for the period compared to negative US$817 million during the first half of2014. Cash outflows in finance leases under construction for the first half of 2015 decreased significantly to US$394million compared to US$1,370 million in the year-ago period taking into consideration the decreasing investments in thefully consolidated FPSOs Cidade de Maricá, Saquarema, Ilhabela and Turritella.

Directional¹ capital expenditure through the first half of 2015 amounted to a combined total of US$265 million, reflectingthe advanced construction progress of the Company’s main projects which are expected to be completed over the nexttwelve months. These amounts correspond to the SBM Offshore share in SBM Inc. (the Company’s constructionsubsidiary) costs as well as costs directly incurred at the joint venture level.

The remaining Directional¹ capital expenditures for the three finance lease vessels under construction is expected to totalapproximately US$265 million, with approximately 75% falling in the second half of 2015. Directional¹ capital expenditureexcludes changes in net working capital and is presented net of upfront payments for FPSOs Cidade de Maricá andCidade de Saquarema.

Further financial information is provided in the consolidated interim financial statements included in this press release.

1 Directional view is a non-IFRS disclosure, which assumes all lease contracts are classified as operating leases and all vessel joint ventures areproportionally consolidated.

Analyst Presentation & Conference Call

SBM Offshore has scheduled a webcast of its presentation to the financial community and a conference call followed by aQ&A session at 19.30 Central European Summer Time on Wednesday, August 5, 2015.

The presentation will be hosted by Bruno Chabas (CEO), Peter van Rossum (CFO), Philippe Barril (COO) and ErikLagendijk (CGCO). Interested parties are invited to listen to the call by dialling +31 20 716 8256 in the Netherlands, +44203 427 1918 in the UK or +1 646 254 3367 in the US. Conference ID: 1511299. Interested parties may also listen to thepresentation via webcast through a link posted on the Investor Relations section of the Company’s website.

A replay of the conference call will be available shortly after the end of the conference call. The replay can be accessedby dialling +31 20 708 5013 and using access code 1511299 until August 19, 2015. The webcast replay will also beavailable on the Company’s website.

| Financial Calendar | Date | Year |

| Extraordinary General Meeting of Shareholders | November 4 | 2015 |

| Trading Update Q3 2015 – Press Release | November 11 | 2015 |

| Full-Year-2015 Results – Press Release | February 10 | 2016 |

| Publication of AGM Agenda | February 23 | 2016 |

| Annual General Meeting of Shareholders | April 6 | 2016 |

Corporate Profile

SBM Offshore N.V. is a listed holding company that is headquartered in Schiedam. It holds direct and indirect interests in other companies that collectively with SBM Offshore N.V. form the SBM Offshore group (“the Company”).

SBM Offshore provides floating production solutions to the offshore energy industry, over the full product life-cycle. The Company is market leading in leased floating production systems with multiple units currently in operation and has unrivalled operational experience in this field. The Company’s main activities are the design, supply, installation, operation and the life extension of Floating Production, Storage and Offloading (FPSO) vessels. These are either owned and operated by SBM Offshore and leased to its clients or supplied on a turnkey sale basis.

Group companies employ approximately 7,000 people worldwide.