SBM Offshore is pleased to report revenues and EBITDA in line with expectations, concluding a year of many achievements notwithstanding the backdrop of the prolonged market downturn. After adjusting to the new market circumstances, the offshore industry shows early signs of stabilization but with a slow recovery. SBM Offshore has continued to transform itself to address this change, safeguarding experience to reinforce a strategic position underpinned by strong cash flow from the Lease & Operate portfolio. At the end of the year the Company was awarded contracts by ExxonMobilfor a Floating Production, Storage and Offloading vessel (FPSO) for development and production in Guyana, subject to Final Investment Decision; the only major new FPSO-related contracts awarded in the industry as a whole in 2016. During the year three FPSOs were delivered to clients, which were successfully integrated into the fleet. These new vessels further strengthened cash flow allowing the company to re-initiate the dividend and complete a significant EUR 150 million share repurchase program during 2016. Given its continued positive outlook for underlying cash flow generation, the Company proposes a cash dividend of US$0.23 per share, an increase of c. 10% year-on-year. In addition the Company will be updating and reinforcing its dividend policy.

Bruno Chabas, CEO of SBM Offshore, commented:

“Experience matters. This was demonstrated by SBM Offshore teams once more this year. Three technologically complex FPSOs were delivered, on time, in line with clients’ expectations, using teams across the globe. SBM Offshore is approaching 300 years of cumulative operating experience and has now delivered 118 Turnkey projects, including 34 FPSOs. And since 1959 the Company has delivered more than 450 offshore terminals. Lease and Operate continues to show solid performance with a fleet that has a production capacity of 1.6 million barrels per day.

To firmly position the Company for the future and align its business with today’s reality in the oil services industry which is characterized by “lower for longer” activity, SBM Offshore initiated a strategic improvement program. This program leverages our experience and is structured around the pillars “Optimize”, “Transform” and “Innovate”. The importance of working closely with client teams to optimize developments combined with the ability to deliver projects on time and on budget has become crucial. As such, with its balance sheet and experienced staff, SBM Offshore is uniquely positioned to create value for customers and investors in today’s oil price environment and thereby utilize its solid foundation for future growth.”

Financial Highlights

- Underlying[1]Directional[2]EBITDA of US$778 million and Underlying Directional EPS of US$0.71 per share

- Directional revenue of US$2,013 million

- Restructuring cost savings of US$260 million, including foreign exchange rate impact; ahead of plan to date

- Cash return to shareholders totaling US$211 million for the year in the form of dividend and share repurchases

- Cash dividend of US$0.23 per share for 2016, a c.10% increase compared to 2015

- Proportional net debt at year-end unchanged at US$3.1 billion, and cash/undrawn credit facilities of US$1.9 billion

- 2017 Guidance: Directional revenue around US$1.7 billion, Directional EBITDA around US$ 750 million

- Recorded adjustments to accounts in-line with 2016 Year-end Update

As reported in the 2016 Year-End Update in December, the 2016 results include a number of non-cash adjustments as a result of its regular year-end review taking into account uncertainties in its outlook for some areas of its operations reflected in its updated business planning assumptions. These adjustments comprise US$90 million in total for the impairment of the Company’s net investment in the Angolan construction yard Paenal and the recognition of an onerous contract for theDSCVSBM Installer. During 2016, the compliance related Brazilian settlement provision was increased by US$36 million, consisting of US$22 million plus a time value of money adjustment[3]of US$14 million. All these amounts have been used to adjust the results for 2016, to arrive at the underlying figures as reported above and throughout this document. 2015 underlying results reflect an adjustment for compliance related items amounting to US$157 million.

Project Review

FPSO

The Company delivered three complex FPSOs to clients during the year. First, FPSOCidade de Maricá(Brazil) was formally on hire as of February 7, 2016 with an initial charter contract of 20 years. Second, FPSOCidade de Saquarema(Brazil) was on hire as of July 8, 2016 with an initial charter contract of 20 years. Third, FPSOTurritella(US Gulf of Mexico) was on hire as of September 2, 2016 with an initial lease and operate contract for 10 years with future extension options up to a total of 20 years.

The FPSOMarlim Sulreceived a decommissioning day rate through the end of the first quarter 2016, and was subsequently formally decommissioned in April 2016 and is currently laid-up in Malaysia.

Turrets Mooring Systems

Commissioning continues in accordance with clients’ schedules and contractual planning, for the two large, complex turrets forPreludeFLNGand FPSOIchthys.

Front-End Engineering and Design (FEED) contracts

On December 20, 2016 the Company announced the award by ExxonMobil of FPSO contracts for the Liza development in Guyana, subject to final investment decision. The Company is progressing with the scope for this FEED study.

Directional Backlog

Directional backlog at the end of December 2016 remained high at US$17.1 billion compared to US$18.9 billion at the end of 2015. This reflects both the lower level of order intake for the Turnkey segment and the resilience of the Lease and Operate portfolio amounting to US$ 17.0 billion at the end of 2016. Revenue generated in 2016 was $2,013 million with total order intake of US$186 million, including US$110 million of new orders in Turnkey.

Funding

At the end of the year, SBM Offshore had cash and undrawn committed credit facilities totaling US$1,904 million compared to US$2,681 million at year-end 2015 on an IFRS basis. On a proportional basis the period ended at US$1,850 million versus US$2,155 million at the end of 2015.

SBM Offshore completed the procedure for re-flagging of the FPSOsCidade de MaricáandCidade de Saquaremaenabling the release of the pre-completion guarantees associated with FPSOsCidade de MaricáandCidade de Saquarema, which were confirmed in November 2016 and January 2017, respectively. As of year-end 2016, no other pre-completion guarantees relating to project financing were outstanding.

Despite the increase in debt associated with the FPSO deliveries to the fleet, the cash requirement for funding the 2016 dividend and share repurchase program, cash flow generation from Lease and Operate was sufficiently strong to maintain the proportional net debt level at US$3.1 billion at year-end.

Transformation, retaining experience

SBM Offshore has transformed itself over the last 3 years in response to the change in market circumstances, while retaining experience. Over this period, the Company has reduced its staff and contractor headcount by more than 50%. Compared to 2014 and as of year-end 2016, this multi-year restructuring has generated approximately US$260 million to date or US$160 million of annual Employee Benefits savings after adjusting for positive foreign exchange rate impacts. This result represents both an acceleration and outperformance as compared to the initial target. An additional amount of approximately US$20 million of annual savings is expected next year as a result of 2016 restructuring.

SBM Offshore has decided to safeguard its experience through retention of core capacity which represents an investment for the future; when the offshore market comes back. However, should the market downturn persist, the Company will consider additional measures to adjust its cost structure.

Operational Update

The Lease & Operate fleet uptime performance for the year was 96.8%. Operational uptime for the full year was impacted during the second quarter by downtime associated with the Deep Panuke production facility. Deep Panuke experienced a flare stack malfunctioning which was repaired in May 2016. Whilst the operational downtime at Deep Panuke affected operational performance it did not materially affect contractual income under the terms of the lease and operate contract.

Shareholder returns

SBM Offshore reached a positive free cash flow inflexion point in the first half of 2016. Given this cash flow position and the outlook for underlying cash generation, the Company decided to return an aggregate c. US$211 million during 2016 to its shareholders representing approximately US$ 1 per share in the form of the dividend and a share repurchase program.

In the second half of the year, a EUR 150 million share repurchase program was announced and subsequently completed. On December 20, the program finished with the repurchase of 11.44 million shares, representing approximately 5% of the original number of outstanding shares and an investment of US$166 million cash. During the Annual General Meeting (AGM) of Shareholders on April 13, 2017, a consequent proposal for cancellation of shares will be made.

With the announcement of Full Year results 2015, SBM Offshore re-initiated its dividend program and paid US$45 million in cash to its shareholders. This dividend represented 25% of Underlying Directional net profit and was US$0.21 on a per share basis.

Considering its continued positive underlying cash flow outlook, the Company proposes a dividend of US$0.23 per share in respect of 2016, to be declared at the AGM on April 13, 2017. This is a c. 10% increase per share compared to last year and represents a pay-out of approximately 30% of the Underlying Directional 2016 net result, adjusted for exceptional items. The proposed ex-dividend date is April 19, 2017. The dividend is payable within 30 days following the AGM.

The annual dividend will be calculated in US Dollars, but will be payable in Euros. The conversion into Euros will be effected on the basis of the exchange rate on April 13, 2017. Given the Company’s strong cash position, the dividend will be fully paid in cash.

SBM Offshore intends to revise its dividend policy relating to future dividend proposals as follows: “The Company’s policy is tomaintain a stable dividend which grows over time. Determination of the dividend is based on the Company’s assessment of the underlying cash flow position and of ‘Directional net income’, where a target payout ratio of between 25% and 35% of ‘Directional net income’ will also be considered”. The proposed change will be presented for discussion at the AGM on April 13, 2017.

Management Board

On November 30, 2016, at an Extraordinary General Meeting of Shareholders, Mr. D.H.M. Wood was appointed as Management Board member and Chief Financial Officer (CFO). Mr. Wood is appointed for a period of four years until the Annual General Meeting of Shareholders in 2021. Mr. Wood succeeded Mr. P.M. van Rossum who retired as Management Board member and CFO.

Corporate Social Responsibility

SBM Offshore has continued to improve its Process Safety performance and has achieved its best ever performance for the most severe Loss of Primary Containment (Tier 1) events since 2014. In Occupational Safety, the outstanding performance recorded in the Turnkey segment was offset by incidents related to the start-up of the three new FPSOs. As a result, the Company was not able to further improve on its robust performance in 2014 and 2015 and the Total Recordable Injury Frequency Rate (TRIFR) stood at 0.31 at the end of 2016, compared to target of below 0.27. The Company is targeting a reduction in safety-related events and is committed to addressing underlying challenges to come back to its solid safety performance as recorded for 2014 and 2015.

Environmental reporting was significantly improved by more accurate data gathering and monitoring of the actual gas composition on each unit to calculate the greenhouse gas (GHG) emission levels for 2015 and 2016. This has resulted in decreases in recorded emissions levels, leading the Company to use revised 2015 reported environmental data for comparisons.

The total volume of gas flared in 2016 remained similar to that for 2015, as revised, notwithstanding three new FPSOs being added to the fleet. Relative to the Company’s increased hydrocarbon production, gas flared was reduced by 23% compared to 2015. Also total GHG emissions relative to hydrocarbon production decreased by 13% compared to 2015. The start-up of the three new FPSOs only increased energy consumption per hydrocarbon production by 3%. Both GHG emissions and energy consumption ratios show better performance than the benchmark International Association of Oil and Gas Producers (IOGP) industry average.

The Company’s sustainability performance continues to improve. For the seventh consecutive year the Company was included in the Dow Jones Sustainability World index, showing SBM Offshore to be an Industry Leader for 2016/2017. This continuous improvement is a credit to the Company’s strong commitment and its sustainability programs on Environmental, Social and Governance (ESG) issues driving to create a more sustainable business.

Compliance

In 2016, further progress was made with the discussions with Brazilian authorities and Petrobras. On July 16, 2016 a Leniency Agreement was signed between Brazilian authorities, Petrobras and SBM Offshore, that will become legally binding after approval by Brazilian Fifth Chamber. Until then, the Company is not under any obligation to make payments under the Leniency Agreement. The Fifth Chamber did not approve the agreement in its current form after which appeals were filed by various governmental parties who were signatories to the Leniency Agreement. Subsequently, the Higher Council decided on December 14, 2016 not to accept appeals filed by the MPF and the General Counsel for the Republic and referred the case back to the Fifth Chamber and the prosecutor handling the case for further review and determination of next steps.

SBM Offshore remains committed to engage with the prosecutor and the Fifth Chamber until the Leniency Agreement is approved by the Fifth Chamber. The Leniency Agreement further remains subject to review by the Federal Court of Accounts but this is not a condition precedent to the Leniency Agreement.

The Company continues to cooperate with the United States Department of Justice following the reopening of the investigation it had closed in November 2014 and its inquiry into Unaoil, a company that SBM Offshore had engaged with as an agent prior to 2012 in relation to delivery of barges, offshore terminals and maintenance.

Outlook and Guidance

Management’s expectations for order intake in 2017 remain unchanged, aligned with an outlook for the industry where recovery is expected to be gradual as clients remain cautious regarding investment in their development programs. At the same time, productive client discussions continue to take place to make deep water projects competitive in today’s oil price environment. A positive medium to long-term outlook is maintained as deep water offshore is expected to remain an important element in the energy supply of the future.

The Company is providing 2017 Directional revenue guidance of around US$1.7 billion, with around US$1.5 billion from Lease and Operate and around US$200 million from Turnkey. 2017 Directional EBITDA is guided at around US$750 million.

FINANCIAL REVIEW

Overview

Directional

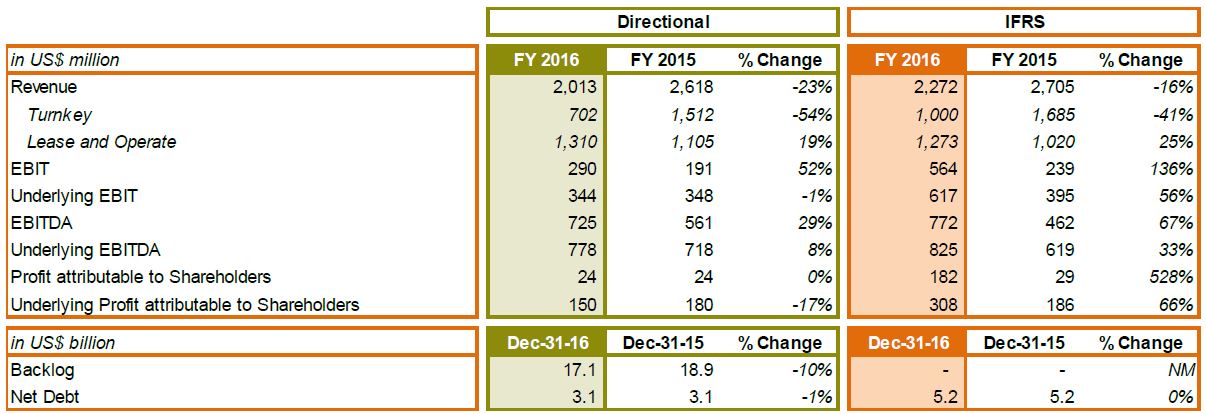

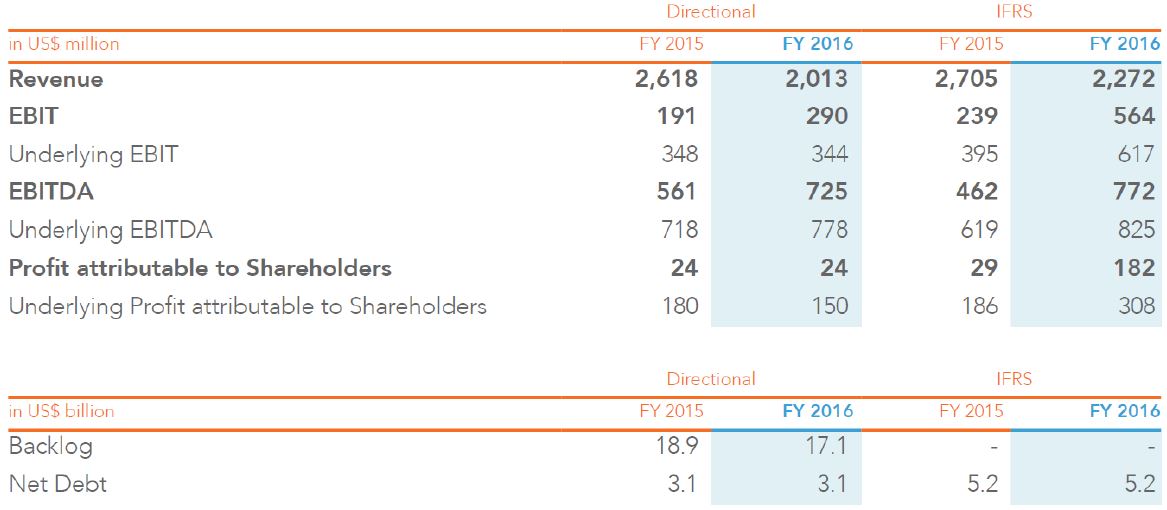

Directional consolidated net income for 2016 was US$ 24 million, stable compared to 2015. This result includes non-recurring items which generated a net loss of US$ 126 million in 2016 compared to a net loss of US$ 157 million in 2015. Excluding non-recurring items, 2016 Underlying consolidated Directional net income attributable to shareholders stood at US$ 150 million, a decrease from US$ 30 million from the previous year, mainly attributable to lower Turnkey segment activity.

Non-recurring items for 2016 underlying performance relate to (i) provision for an onerous long-term charter contract with the Diving Support and Construction Vessel (DSCV)SBM Installer(US$ 31 million), (ii) the update of the provision for contemplated settlement with Brazilian authorities and Petrobras (US$ 36 million) and the impairment of the Company’s carrying amount for the net investment in the Joint Venture owning the Paenal construction yard (US$ 59 millions). These non-recurring items are the same in both IFRS and Directional, impacting EBIT and EBITDA by US$ 53 million, net financing costs by US$ 14 million and Share of Profit of Equity-accounted investees by US$ 59 million. For reference, non-recurring items for 2015 totalling US$ 157 million, were included in EBIT and EBITDA and were related to compliance issues.

Directional earnings per share (EPS) in 2016 amounted to US$ 0.11 compared to US$ 0.11 per share in 2015. Adjusted for non-recurring items, Underlying Directional EPS decreased by 17% year-on-year from US$ 0.85 in 2015 to US$ 0.71.

New orders for the year totaled US$ 110 million as a result of current market downturn, which compares to US$ 248 million achieved in 2015.

Directional revenue decreased by 23% to US$ 2,013 million compared to US$ 2,618 million in the year-ago period. This was primarily attributable to lower Turnkey segment revenues.

Directional backlog at the end of 2016 remained high at US$ 17.1 billion compared to US$ 18.9 billion at the end of 2015. This reflects both the lower level of order intake for the Turnkey segment and the resilience of the Lease and Operate portfolio amounting to US$ 17.0 billion at the end of 2016.

Directional EBITDA amounted to US$ 725 million, representing a 29% increase compared to US$ 561 million in 2015. This figure includes non-recurring net costs totaling US$ 53 million.

Directional EBIT increased to US$ 290 million after non-recurring net costs of US$ 53 million. This compares to US$ 191 million in 2015 which included US$ 157 million of non-recurring costs.

IFRS

Reported consolidated 2016 IFRS total net income was US$ 247 million versus US$ 110 million in 2015. IFRS net income attributable to shareholders amounts to US$ 182 million compared to US$ 29 million in 2015.

IFRS revenue decreased by 16% to US$ 2,272 million versus US$ 2,705 million in 2015. This was mainly attributable to lower Turnkey segment revenues.

IFRS EBITDA amounted to US$ 772 million, representing a 67% increase compared to US$ 462 million in 2015.

IFRS EBIT increased to US$ 564 million, representing 136% increase compared to US$ 239 million in 2015.

IFRS Net Debt at the year-end totaled US$ 5,216 million versus US$ 5,208 million in 2015. All bank covenants were met and available cash and undrawn committed credit facilities stood at US$ 1,537 million.

Financial Highlights

The year was marked by the following financial highlights:

- Successful delivery of FPSOsCidade de Maricá,Cidade de SaquaremaandTurritellawhich were formally on hire respectively as of February 7, 2016, July 8, 2016 and September 2, 2016.

- The Company completed its share repurchase program under the authorization granted by the Annual General Meeting of Shareholders of the Company held on April 6, 2016. In the period between August 11, 2016 and December 20, 2016, a total number of 11,442,179 shares totaling EUR 150 million were repurchased. The repurchased shares are held as Treasury shares predominantly for share capital reduction purposes and, to a lesser extent, for employee share programs.

- Award of the Front End Engineering and Design component of the contract for a FPSO by Esso Exploration and Production Guyana Limited to the Company and for which construction, installation and operation of the FPSO remain subject to a final investment decision expected in 2017. This contributed to new orders of US$ 110 million in aggregate.

- The Company, together with its core relationship banks, signed an amendment of its Revolving Credit Facility (RCF) on April 18, 2016, providing headroom improvements to the leverage and interest coverage ratios. The agreed upon amendments, combined with a strong cash position, provide the Company with a greater degree of flexibility in navigating the current industry downturn.

- During the first half of 2016, the Company, the Ministry of Transparency, Oversight and Control (Ministério da Transparência, Fiscalização e Controle – ‘MTFC’), the Attorney General’s Office (Advocacia-Geral da União – ‘AGU’), the Public Prosecutor’s Office (Ministério Público Federal –‘MPF’) and Petrobras engaged in further negotiations which resulted in the signature on Friday, July 15 of a Settlement Agreement (‘Leniency Agreement’). As a result, the provision booked in December 2015 has been increased in the consolidated financial statements as at December 31, 2016, up to the amount of the present value of the financial terms of the leniency agreement being US$ 281 million, impacting the lines “Other operating expense” of the consolidated income statement by US$ 22 million and ‘Net financing costs’ by US$ 14 million for the unwinding of the discounting impact of future settlement. As more fully explained in section 5.3.1 Highlights of the Annual Report, the agreement will become legally binding after approval of the Fifth Chamber for Coordination and Review and Anti-Corruption of the Federal Prosecutor Service and remains subject to review by the Federal Court of Accounts (‘TCU’), which is not a condition precedent to the Leniency Agreement. However, the terms of this agreement remains SBM Offshore’s current best estimate for an eventual settlement, given that it was duly signed by the relevant parties and the approval process is still underway.

- At the end of January 2016, the United States Department of Justice (DoJ) informed the Company that it has re-opened its past inquiry of the Company in relation to the alleged improper sales practices over the period 2007 to 2011 and has made information requests in connection with that inquiry. During the period, the Company has cooperated with the DoJ and remains committed to close out discussions on this legacy issue which the Company self-reported to the authorities in 2012 and for which it reached a settlement with the Dutch Public Prosecutor in 2014. The Company also continues to cooperate with the DoJ for its inquiries in Unaoil, a company that SBM Offshore had engaged with as an agent prior to 2012 in relation to delivery of barges, offshore terminals and maintenance.

- As a result of an on-going review of the cost structure and continued market downturn, the Company’s workforce reduction over 2016 totaled approximately 2,250 positions. Roughly 650 were full-time employees and contractor staff. The remaining 1,600 were construction yard positions related to demobilization following successful delivery of main projects over the period. Restructuring costs of US$ 37 million were recorded during the period. The adaptation to market developments is focused on retaining core competencies.

- The Company has a long-term charter contract with the Diving Support and Construction Vessel (DSCV)SBM Installer. Due to the ongoing downturn which has created significant over-supply in offshore markets, the costs of the long-term chartering contract exceed the economic benefits expected to be received by the Company through the utilization of the vessel. As a result, a provision for onerous contract of US$ 31 million has been recognized over the period.

- The activity outlook for the Company’s investment (30% ownership) in the Joint Venture owning the Paenal construction yard operating in Angola has deteriorated. As a result, the Company’s carrying amount for the net investment in this entity has been impaired by US$ 59 million on the second half of 2016. Because this investment is consolidated using the equity method, this non-cash impairment is recognized in the Company’s Consolidated Income Statement on the line item ‘Share of profit of equity-accounted investees’.

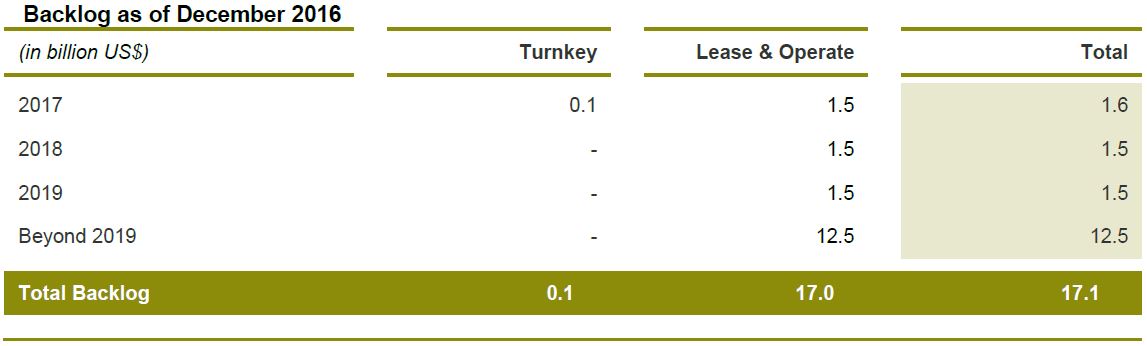

Backlog

Directional backlog at the end of 2016 remained healthy at US$ 17.1 billion compared US$ 18.9 billion at the end of 2015. This reflects both the lower level of order intake for the Turnkey segment and the resilience of the Lease and Operate portfolio.

Directional Turnkey backlog decreased to US$ 0.1 billion compared to US$ 0.5 billion in 2015 as no major Turnkey orders were signed in 2016. As market conditions continued to be challenging during the period, the level of tendering activity was lower than in 2015 and the order intake continued to be impacted by structural delays in client final investment decisions.

Backlog as of December 31, 2016 is expected to be executed as per the below tables:

Revenue

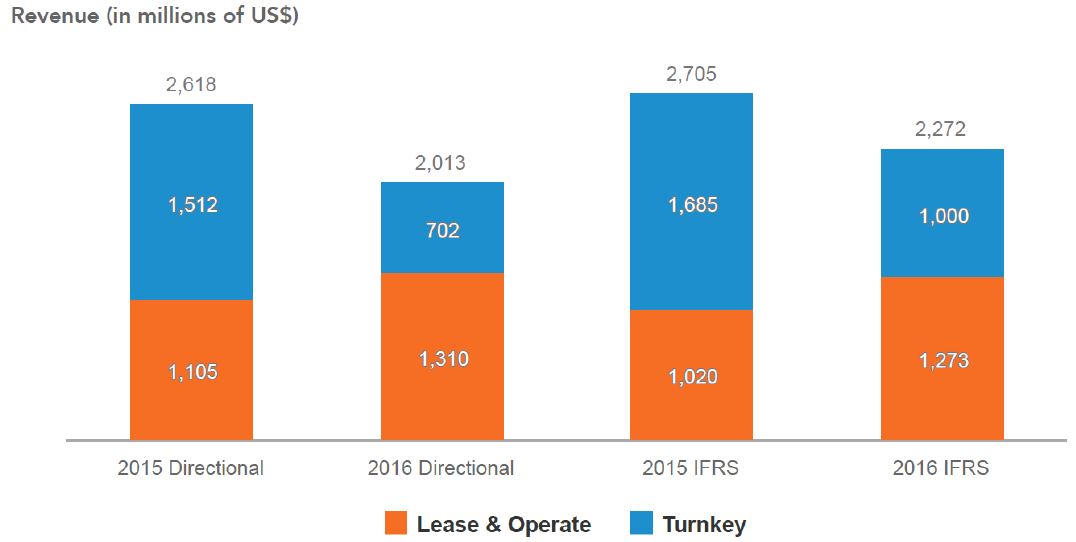

Directional Revenue decreased by 23% year-on-year despite an increase of 19% for the Lease and Operate segment:

Directional

Third party Directional Turnkey revenue came down 54% year-over-year to US$ 702 million, representing only 35% of total 2016 revenue. This compares to US$ 1,512 million, or 58% of total revenue, in 2015. The decrease is mostly attributable to the completion stage reached in the course of 2016 on Ichthys turret and FPSOsCidade de Maricá, Cidade de SaquaremaandTurritella, as well as the very low order intake in 2014, 2015 and 2016 as a result of the market downturn.

Directional Lease and Operate revenue increased by 19% to US$ 1,310 million, representing 65% of total Directional revenue contribution in 2016, up from the 42% contribution of 2015. The increase in segment revenue is attributable to the start-up of FPSOsCidade de Maricá, Cidade de SaquaremaandTurritellawhile no vessel have been decommissioned during the period.

IFRS

Total IFRS revenue decreased during the year, down by 16% to US$ 2,272 million, despite an increase of 25% for the Lease and Operate segment. This was mainly attributable to significantly lower revenue recognized in the Turnkey segment upon completion of major projects in the course of 2016 as well as low order intake in 2014, 2015 and 2016.

Profitability

The Company’s primary business segments are Lease and Operate and Turnkey plus ‘Other’ non-allocated corporate income and expense items. EBITDA and EBIT are analyzed by segment but it should be recognized that business activities are closely related, and that certain costs are not specifically related to either one segment or another. For example, when sales costs are incurred, including significant sums for preparing a bid, it is often uncertain whether the project will be leased or contracted on a turnkey lump sum basis.

The Company’s profitability may be affected by external variables and conditions. Profitability may be sensitive to significant areas of estimation and judgements, and to potential interest rates and currency fluctuations against the US dollar as described in the Annual Report notes 5.2.7.B (a) and 5.3.29 to the financial statements, respectively.

In recent years, new lease contracts are showing longer duration and are systematically classified under IFRS as finance leases for accounting purposes whereby the fair value of the leased asset is recorded as a Turnkey ‘sale’ during construction. For the Turnkey segment this has the effect of accelerating during the construction period a substantial part of the lease profits which would in the case of an operating lease be recognized through the Lease and Operate segment during the lease period. To address this lease accounting issue and IFRS 10 and 11 standards introduced in 2014, the Company has, in addition to its IFRS reporting, assessed its performance by treating all lease contracts as operating leases and consolidated all JVs related to lease contracts on a proportional basis, referred to as Directional. This provides consistency in segment presentation.

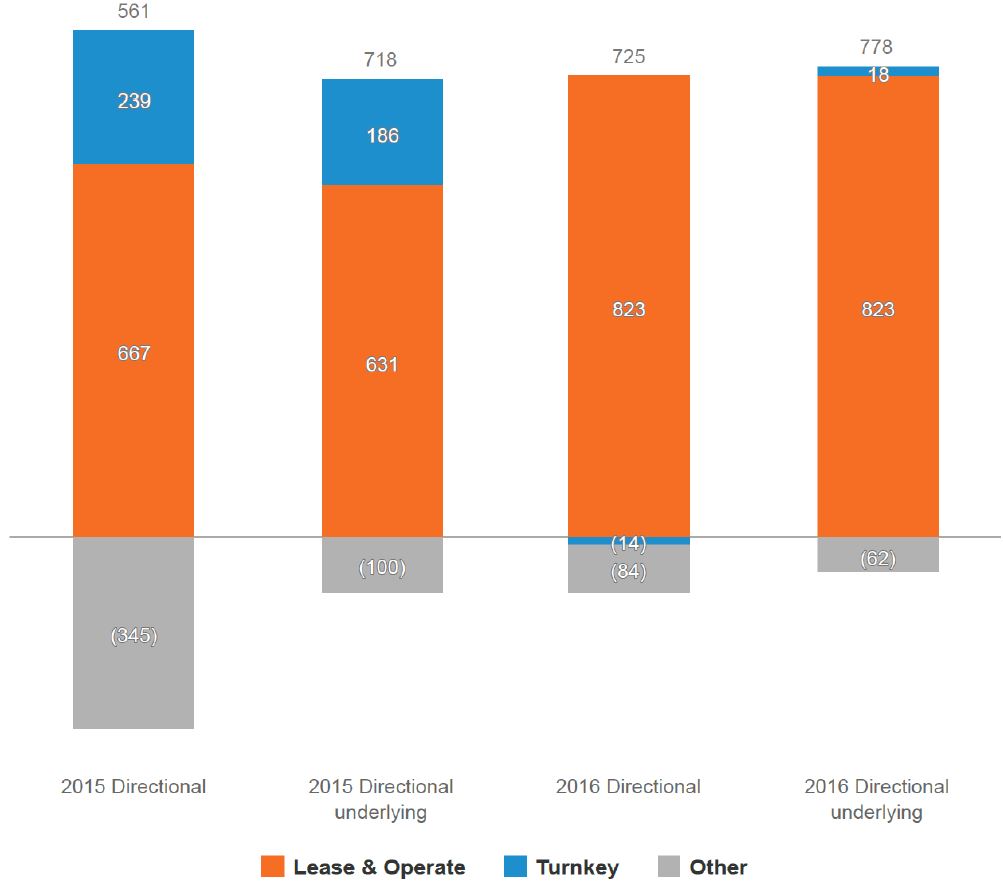

EBITDA Directional (in millions of US$)

Reported 2016 Directional EBITDA was US$ 725 million compared to US$ 561 million in 2015. Directional EBITDA consisted of US$ 823 million from the Lease and Operate segment compared to US$ 667 million in 2015, and a loss of US$ 14 million from the Turnkey segment compared to profit of US$ 239 million in 2015.

Other non-allocated expenses came at US$ 84 million, compared to US$ 345 million in 2015, related mainly to restructuring charges and update of provision related to potential settlement contemplated with the Brazilian authorities and