Solid Turnkey Performance; Cost Savings Ahead of Plan; Positive Free Cash Flow Generation; EUR 150 Million Share Repurchase

SBM Offshore is pleased to report revenue in line with expectations, a Settlement Agreement with Petrobras and Brazilian authorities, the delivery of two of three vessels under construction and FPSO Turritella approaching Ready for Start-Up leading to first oil. The revenue contribution from the new additions to the Lease & Operate fleet has allowed the Company to commence generating positive free cash flow in the first half of the current fiscal year, which is expected to be continued over the remainder of 2016. While the oil and gas industry continues to face headwinds, SBM Offshore is playing its part to lower the cost of deepwater development. These advances have led to increased client engagement and positive signs for the medium term outlook of the offshore industry. The Company reiterates its 2016 guidance and announces the initiation of a EUR 150 million share repurchase program.

Bruno Chabas, CEO of SBM Offshore, commented:

“Industry challenges persisted in the first half of 2016 although more productive discussions with some clients to find economic solutions for deepwater development are taking place. We are making significant progress in aligning our business to the realities of today’s market. In addition, we are building on our proven track record of on time delivery through investments in our Fast4ward initiative actively positioning the Company to remain the provider of choice in the floating solutions business. The importance of experienced and reliable contractors takes center stage. SBM Offshore remains disciplined in its commercial approach to new projects in order to mitigate risks which could adversely impact the Company in the years ahead.”

Financial Highlights

- Share repurchase program of EUR 150 million announced

- Cost savings of US$270 million, well ahead of plan

- New Chief Financial Officer nominated

- Settlement Agreement reached in Brazil

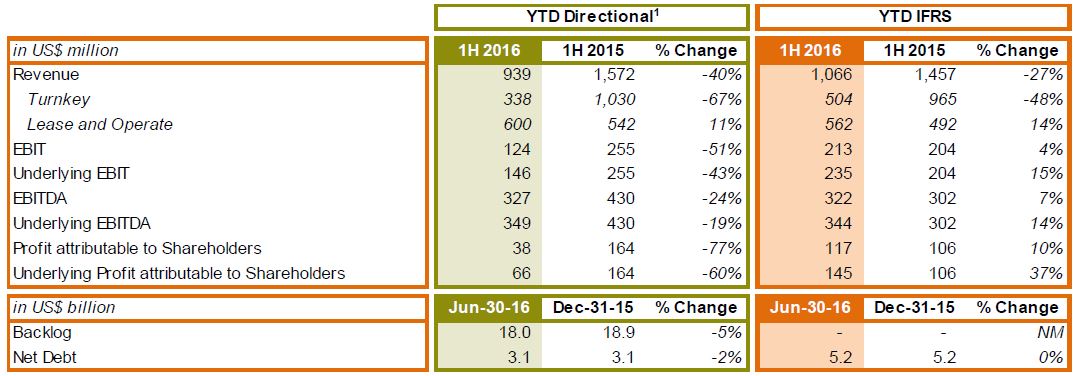

- Directional[1] revenue in line with expectations at US$939 million

- Underlying Directional[1] EBITDA of US$349 million and underlying EPS of $0.31 per share

- Proportional net debt at the end of June reduced by US$68 million to US$3.1 billion

- Cash dividend of US$0.21 per share paid on May 3, 2016

FIRST HALF 2016 RESULTS

Guidance

The Company reiterates its 2016 Directional[1] revenue guidance of at least US$2.0 billion, of which US$0.6-0.7 billion is expected in the Turnkey segment and US$1.3-1.4 billion in the Lease and Operate segment. The Company also reconfirms the 2016 Directional[1] EBITDA guidance of around US$750 million.

Overview

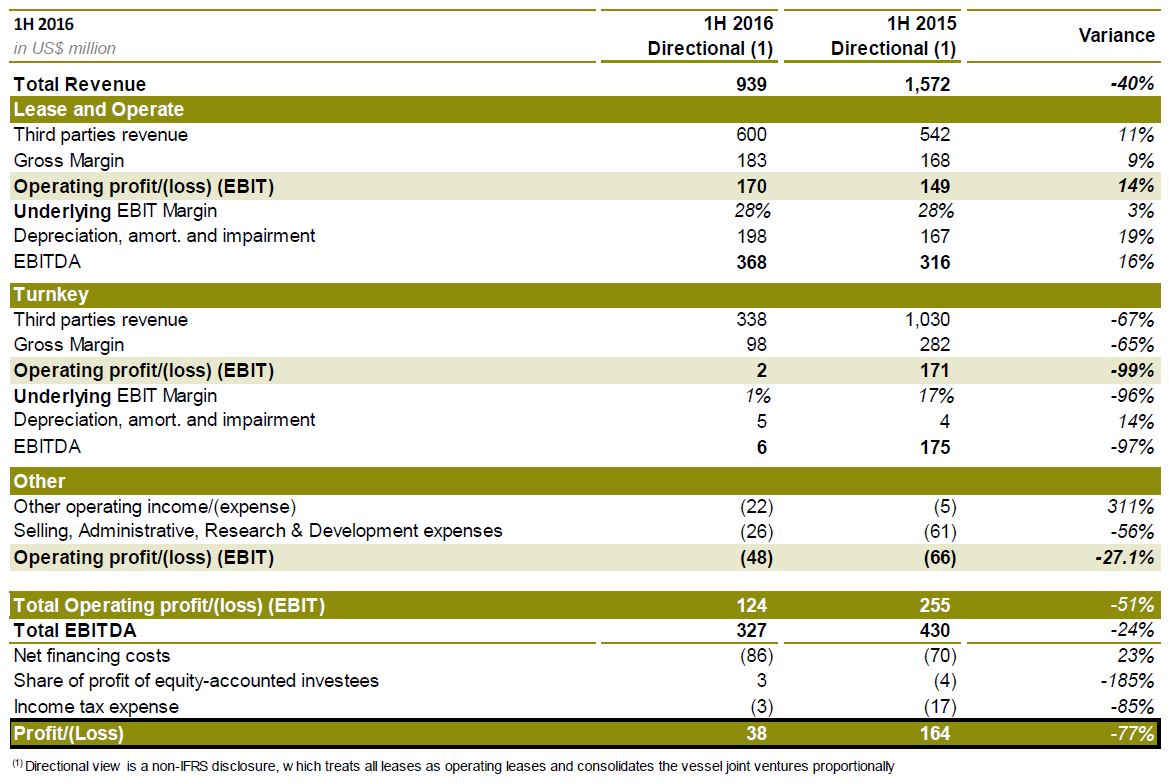

Directional[1] revenue for the first half of 2016 declined by 40% to US$939 million versus US$1,572 million in the year-ago period, reflecting the expected slowdown in Turnkey activity levels due to continued difficult oil and gas market conditions.

Directional[1] Turnkey revenue decreased by US$692 million from the year-ago period to US$338 million for the first half of 2016. This reflects lower activity on the construction of the FPSOs Cidade de Maricá, Cidade de Saquarema and Turritella, the finalization of the remaining turret projects, the positive effect in 2015 of the divestment of a 45% stake in the Turritella project to joint venture partners and the lack of significant order intake over the periods.

Directional[1] Lease and Operate revenue increased by 11% versus the first half of 2015 mainly due to the commencement of production of FPSO Cidade de Maricá which was on hire commencing February 7, 2016 and the contribution of the Production Handling Agreement signed in September 2015 with Noble to connect the Big Bend and Dantzler fields to the Thunder Hawk DeepdraftTM Semi in the U.S. Gulf of Mexico.

HSSE

The Company has continued to improve its safety performance in the first half of 2016. Reported Total Recordable Injury Frequency Rate (TRIFR) was on target at 0.26, reflecting the lower number of incidents and manhours due to project construction completion.

Process Safety Management activities continued, including strengthening Management of Change controls and improving the information requirements for Process Safety for each operating unit.

As it relates to environmental performance, the volume of oil discharged through produced water has continued to be consistently better than the industry benchmark. Flaring under the Company’s control increased above target due to the flaring on new units in Brazil as well as one in Angola. In the latter case, remedial work on that unit is being scheduled.

Compliance

On July 16, 2016 SBM Offshore announced the signing of a Settlement Agreement totaling US$273 million with the Brazilian Ministry of Transparency, Oversight and Control (Ministério da Transparência, Fiscalização e Controle – “MTFC”), the Public Prosecutor’s Office (Ministério Público Federal – “MPF”), the General Counsel for the Republic (Advocacia Geral da União – “AGU”), Petróleo Brasileiro S.A. – Petrobras (“Petrobras”) closing out the inquiries of the MPF, the MTFC and Petrobras into potentially improper sales practices in Brazil.

Under the terms of the Settlement Agreement the MTFC, the MPF, the AGU and Petrobras fully discharge and exempt SBM Offshore from legal actions for all matters related to or arising from any acts relating to its then main Brazilian agent and his companies over the period 1996 – 2012 and all related investigations conducted by Petrobras, the MPF and the MTFC.

The terms of the Settlement Agreement consist of the following items:

- cash payment by SBM Offshore totalling US$162.8 million, of which US$149.2 million will go to Petrobras, US$6.8 million to the MPF and US$6.8 million to the Council of Control of Financial Activities (Conselho de Controle de Atividades Financeiras – “COAF”). This amount will be paid in three installments. The first installment of US$142.8 million will be payable as of the effective date of the Settlement Agreement. The two further installments of US$10 million in nominal value each will be due respectively one and two years following the effective date of the Settlement Agreement

- a fixed reduction in lease income based on relinquishing 95% in future performance bonus payments related to FPSOs Cidade de Anchieta and Capixaba lease and operate contracts, representing a nominal value of approximately US$179 million over the period 2016 to 2030, or a present value for SBM Offshore of approximately US$112 million

- SBM Offshore further remains under the obligation to cooperate with the procedures that may be conducted by the MTFC and the MPF against third parties

- the implementation by SBM Offshore of improvements of its internal compliance program in relation to Brazil, in consultation with the MTFC, to whom SBM for three years following the effective date of the Settlement Agreement, will periodically report on matters addressed in the agreement.

The Public Prosecutor’s Office submitted the Settlement Agreement for approval of the Fifth Chamber for Coordination and Review and Anti-Corruption of the Federal Prosecutor Service. Upon receiving approval the Settlement Agreement will become binding upon the parties which will trigger the payment of the first installment of US$142.8 million to Petrobras, the MPF and the COAF. The MTFC has also sent the Settlement Agreement to the Federal Court of Accounts (Tribunal de Contas da União – “TCU”).

The Company continues to cooperate with the United States Department of Justice following the reopening of its investigation in January 2016.

Operational Update

First half 2016 Lease & Operate fleet uptime performance was 95%. Operational uptime for the period was mainly impacted by downtime associated with the Deep Panuke production facility and FPSO Cidade de Paraty.

In the Company’s first quarter trading update of May 11, 2016 it was highlighted that the Deep Panuke production facility experienced a malfunctioning of its flarestack on March 20, 2016. The facility was shutdown for repairs which were completed on May 26, 2016, within the 120 day contractual allowance. While there was no impact to the contractual dayrate related to the shutdown, the downtime impacted the fleet uptime average by 3.1%.

Also during the period, FPSO Cidade de Paraty experienced a temporary production interruption due to a compressor malfunction. Contingencies, including a spare compressor, have been put in place to mitigate future impact. Downtime impacted the fleet average by 0.9%.

Furthermore, on June 28, 2016, at an onshore third party natural gas processing facility in Pascagoula, Mississippi, an explosion occurred which led to required intermittent shutdowns of the Thunder Hawk DeepDraft™ Semi in the U.S. Gulf of Mexico due to pipeline capacity constraints. Given the unique nature of the Production Handling Agreement, fees associated with produced volumes could lead to a loss of income.

Project Review

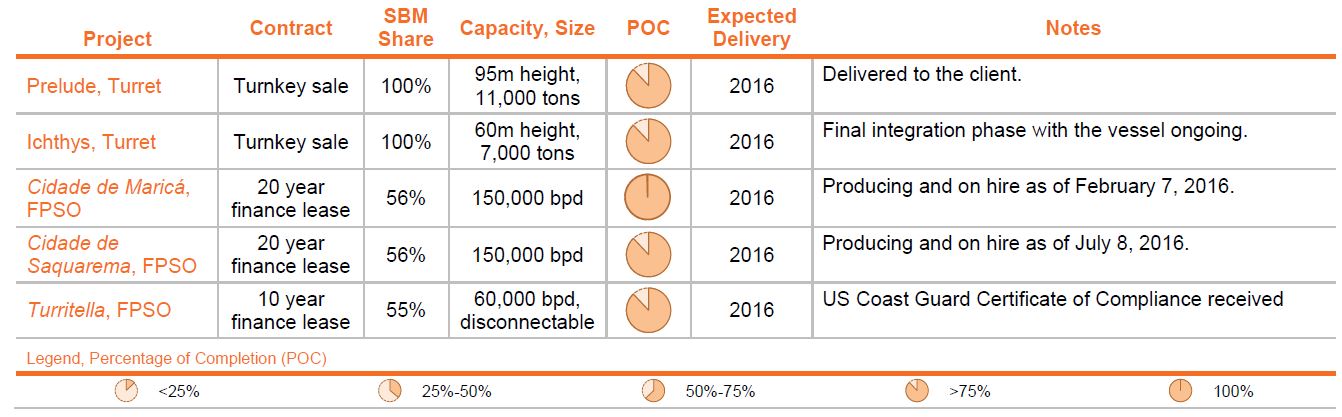

FPSO Cidade de Maricá (Brazil)

On February 16, 2016 SBM Offshore announced that Cidade de Maricá was formally on hire as of February 7, 2016 after achieving first oil and the completion of a 72-hour continuous production test leading to final acceptance.

FPSO Cidade de Saquarema (Brazil)

On July 12, 2016 SBM Offshore announced that Cidade de Saquarema was formally on hire as of July 8, 2016 after achieving first oil and the completion of a 72-hour continuous production test leading to final acceptance.

FPSO Turritella (US Gulf of Mexico)

The vessel is on location in the US Gulf of Mexico and the United States Coast Guard’s Certificate of Compliance was issued on July 29, 2016. Ready for Start-up is the next necessary step in supporting well operations before commercial production and first oil. The charter contract includes an initial period of 10 years with extension options up to a total of 20 years.

FPSO Marlim Sul (Brazil)

Decommissioning activities were completed in April 2016. The vessel received a decommissioning dayrate through the end of the first quarter of 2016.

Sea Lion FPSO FEED (Falkland Islands)

On January 13, 2016 SBM Offshore announced the award of the Front-End Engineering and Design (FEED) contract, by Premier Oil plc, for an FPSO for Phase 1 of its Sea Lion development in the North Falkland Basin. FEED activity continues to progress on the 18-month contract with final investment decision targeted for the second half of 2017.

BrowseFLNGFEED (Australia)

On March 23, 2016, participants in the Browse Floating Liquified Natural Gas (FLNG) project in Australia decided not to proceed with the development. As a result, SBM Offshore’s FEED activities related to the project have ceased.

Turrets & Mooring Systems

Commissioning continues in accordance with client’s schedules and contractual planning for the two large, complex turrets for Prelude FLNG and FPSO Ichthys.

Main Projects Overview

Directional[1] Backlog

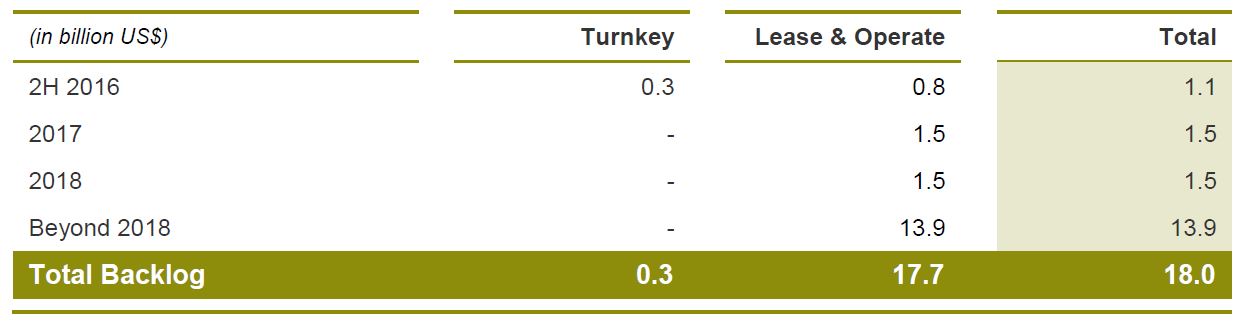

Directional[1] backlog at the end of June 2016 came in at US$18.0 billion compared to US$18.9 billion at the end of 2015. While this reflects US$939 million of revenue generated in the first half of 2016 and the low level of order intake for the Turnkey segment, it also emphasizes the resilience and excellent long-term visibility of the Lease and Operate portfolio revenue.

Directional[1] Turnkey backlog decreased to US$0.3 billion compared to US$0.5 billion at the end of 2015 as no major Turnkey orders were signed in the first half of 2016.

While the price of oil appears to be stabilizing, order intake continued to be impacted by delays in client final investment decisions. New orders during the first half of 2016 amounted to US$48 million. Backlog as of June 30, 2016 is expected to be executed as per the below table:

Funding

As of June 30, 2016, SBM Offshore had cash and undrawn committed credit facilities totaling US$2,122 million compared to US$2,681 million at year-end 2015 on an IFRS basis. On a Proportional basis the period ended at US$2,060 million versus US$2,155 million at the end of 2015.

Proportional net debt as of June 30, 2016 amounted to US$3,079 million versus US$3,147 million at the end of 2015. The improvement over the period is mostly attributable to cash flow generation in the Lease & Operate segment. This was partially offset by ongoing investments in the three FPSOs under construction and the reinstatement of a dividend at US$0.21 per ordinary share.

Investing in the Future

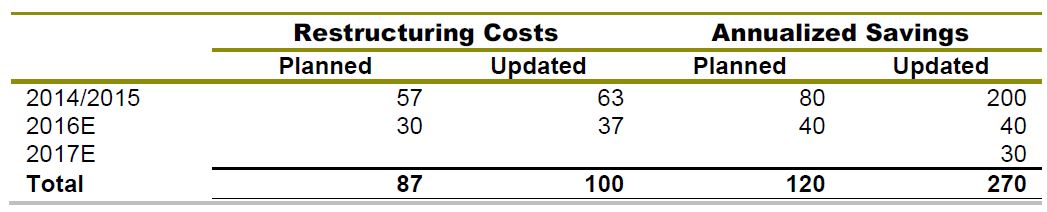

In previous announcements SBM Offshore stated that a planned multi-year restructuring was expected to generate costs totaling US$87 million with anticipated annualized savings of US$120 million as a result of workforce reductions totaling 1,900 positions.

Updated figures show that the Company plans to realize US$270 million of annualized Employee Benefits savings. Excluding the approximately US$80 million in positive impact from foreign exchange rate fluctuations over the period 2014 – 2016, expected savings amount of US$190 million compared to anticipated annualized cost savings of US$120 million. The additional savings include approximately US$20 million due to natural attrition, approximately US$30 million due to increased expected reductions in headcount as a result of the 2016 restructuring plan and approximately US$20 million from various additional cost saving measures.

Building on the good progress achieved on cost savings related to a reduced workload in the Company’s Engineering Centers, attention is now turning towards overheads. Additional cost savings will be targeted through various means, including a 10% voluntary cut in fixed income for the next twelve months by the members of the Management Board and the Executive Committee. In addition, the Management Board and the Executive Committee will reduce their potential 2016 short-term cash incentive by 50%.

The Management Board continues to view a full recovery as unlikely before 2018, and as previously announced the Company will maintain a Turnkey overcapacity to position itself for a future market upturn. This leads to cumulative Directional[1] Turnkey EBIT losses of approximately US$150 million over 2016 and 2017, which is expected to be mostly back-end loaded. SBM Offshore retains the capacity to make further adjustments to its cost based should market conditions warrant.

Uses of Cash and Share Repurchase

The Company has reached the positive free cash flow inflexion point in the first half of 2016. With the delivery of the last vessels under construction, the release of pre-completion corporate guarantees associated with project financings is a top priority. A recent Brazilian court ruling regarding the enforceability of vessel mortgages under Bahamian flag has been cast in doubt. As a result, SBM Offshore is in the process of re-flagging FPSOs Cidade de Maricá and Cidade de Saquarema before the project loans are accepted by the lenders as non-recourse to the parent. This process is expected to be completed early in the fourth quarter of 2016.

Simultaneously, the Company has undertaken reviews of various uses of cash and will continue evaluating the best opportunities for returns on capital and value creation. A first step was taken on April 6, 2016 when the Annual General Meeting of Shareholders voted in favor of the proposed US$0.21 per ordinary share dividend distribution. The cash dividend was paid in Euros on May 3, 2016 using an exchange rate of 1.1368, equating to €0.1847 per ordinary share.

SBM Offshore is pleased to announce a share repurchase program effective August 11, 2016. The Company intends to repurchase shares up to EUR 150 million predominantly for share capital reduction purposes and, to a lesser extent, for employee share programs. The repurchase program is expected to be completed no later than the end of 2016, and it will be accomplished under the authorization granted by the Annual General Meeting of Shareholders of the Company held on April 6, 2016. The execution of the share repurchase program will be done under the terms of an engagement letter with a third party, performed in compliance with the safe harbor provisions for share repurchases, and therefore transactions may be carried out during closed periods. In accordance with theEuropean Market Abuse Regulation,the Companywill inform the market on the progress made in the execution of this program through weekly press releases and updates on its website. The share repurchase program does not obligate the Company to acquire any amount of shares, and it may be suspended at any time at the Company’s discretion.

Master Limited Partnership (MLP)

The contemplated initial public offering of common units is subject to market conditions, which continue to be challenging in the current environment. The Management Board regards the MLP as a key tool in support of funding future awards, and expects the MLP market conditions to improve once the overall confidence in the Oil and Gas market has returned and clients are committing to new investments.

Management Board

Further to the announcement that Mr. P.M. van Rossum will retire as Management Board member and Chief Financial Officer (CFO), the selection process for a replacement has been successfully concluded. The Supervisory Board nominates Mr. D.H.M. Wood as Management Board member and CFO. The Company will hold an Extraordinary General Meeting of Shareholders on November 30, 2016 where it will be proposed that Mr. Wood be appointed as a member of the Management Board for a period of four years until the Annual General Meeting of Shareholders in 2021. Further information regarding this nomination can be found in a separate press release issued today.

Outlook and Guidance

Management’s expectations for low order intake in 2016 and 2017 remain unchanged. Industry challenges affecting the Turnkey segment since 2014 have persisted in the first half of 2016 although green shoots are beginning to appear resulting in more productive discussions with clients on deepwater projects. A positive medium to long-term outlook is maintained as offshore development remains a crucial component of the overall energy mix to meet future demand.

The Company reiterates its 2016 Directional[1] revenue guidance of at least US$2.0 billion, of which US$0.6-0.7 billion is expected in the Turnkey segment and US$1.3-1.4 billion in the Lease and Operate segment. The Company also reconfirms the 2016 Directional[1] EBITDA guidance of around US$750 million.

Full year 2016 Directional[1] capital expenditure for the three finance lease vessels under construction has been revised from approximately US$90 million to approximately US$70 million, in line with revised cost estimates on these projects. Directional[1] capital expenditure excludes changes in net working capital and is presented net of upfront payments for FPSOs Cidade de Maricá and Cidade de Saquarema.

FINANCIAL REVIEW

Highlights – Directional[1] Performance

Directional[1] revenue for the first half of 2016 declined by 40% to US$939 million versus US$1,572 million in the year-ago period, reflecting the strong slowdown in Turnkey activity levels due to continued difficult oil and gas market conditions.

Directional[1] revenue by segment was as follows:

- Directional[1] Turnkey revenue decreased by US$692 million from the year-ago period to US$338 million for the first half of 2016, reflecting lower activity on the construction of the FPSOs Cidade de Maricá, Cidade de Saquarema and Turritella, as well as the finalization of the remaining turret projects during the first half of 2016, the positive effect in 2015 of the divestment of a 45% stake in the Turritella project to joint venture partners and the lack of significant order intake over the periods.

- Directional[1] Lease and Operate revenue increased by 11% versus the first half of 2015 mainly due to FPSO Cidade de Maricá commencing production on February 7, 2016 and the contribution of the Production Handling Agreement signed in September 2015 with Noble to connect the Big Bend and Dantzler fields to the Thunder Hawk DeepdraftTM Semi in the U.S. Gulf of Mexico.

Directional[1] Earnings Before Interest, Taxes, Depreciation and Amortization (EBITDA) for the first half of 2016 decreased to US$327 million compared with US$430 million in the year-ago period. This variance was primarily attributable to:

- Directional[1] Turnkey EBITDA decreased by US$169 million due to the strong drop off of activity on all main construction projects during the period and despite the steady contribution of gross margin expressed as a percentage of Turnkey revenue (29% in the period versus 27% in the first half of 2015).

- Directional[1] Lease and Operate EBITDA increased by 16% compared with the year-ago period mostly due to FPSO Cidade de Maricá commencing production in February 2016. First half 2016 Directional[1] Lease & Operate EBITDA margin came in at 61% compared to 58% during the first half of 2015.

- As a result of the signing of the Settlement Agreement with Petrobras and Brazilian authorities in July 2016, the provision booked in the full-year 2015 financials has been adjusted to reflect the present value of the financial terms of the agreement at US$273 million. This impacts the Other operating expense’ and Net Financing Costs’ lines of the consolidated income statement by US$22 million and US$6 million respectively during the period.

- As a result of the ongoing review of the Company’s cost structure due to the continued market downturn, the workforce reduction is now expected to amount to at least 650 positions worldwide over the course of 2016 as a result of the 2016 restructuring plan. This necessary adjustment of the Company’s structure was initiated at the end of 2014 allowing the Turnkey segment to remain at breakeven during the first half of 2016 and to lower overheads costs by 29% during the period. Restructuring costs accounted for as “Other operating expense” over the period represent a charge of US$31 million. The expected annualized savings are anticipated to reach at least US$70 million as a result of the restructuring plan.

For the first half of 2016, Directional[1] EBIT decreased to US$124 million, compared to US$255 million in 2015.

Directional[1] net financing costs totaled US$86 million in the first half of 2016, up from US$70 million in the year-ago period. The increase was primarily due to interest costs related to the project financing of FPSO Cidade de Maricá, which commenced production in early 2016, and the unwinding of the Brazil provision settlement discount for US$6 million.

The 2016 effective tax rate came in at 7% compared to 9% in the year-ago period.

SBM Offshore recorded a Directional[1] net profit of US$38 million in the first half of 2016 or US$0.18 per share, compared with US$164 million or US$0.78 per share for the first half of 2015.

Adjusted for the increase of the Brazilian settlement provision, underlying Directional[1] net profit amounts to US$66 million or US$0.31 per share.

IFRS Performance

First half 2016 IFRS revenue amounted to US$1,066 million, a decrease of 27% versus US$1,457 million in the year-ago period as a result of the slowdown of construction activities despite the 14% year-on-year increase in Lease & Operate revenue.

IFRS EBIT for the first half of 2016 remained stable to US$213 million compared to US$204 million in the year ago period as the drop of Turnkey gross margin was offset by the sharp decrease of overhead costs and additional Lease & Operate gross margin.

IFRS net income attributable to shareholders came in at US$117 million compared to US$106 million a year ago.

Statement of Financial Position

Total assets increased by US$0.5 billion to US$11.8 billion as of June 30, 2016 compared from US$11.3 billion at year-end 2015. This reflects the finalization of the Company’s investments in FPSOs Cidade de Maricá, Cidade de Saquarema and Turritella during the period, the reduction of working capital and an increased cash position.

As of June 30, 2016 IFRS net debt remained stable at US$5,227 million as a result of strong cash-flow generation offset by a decrease in working capital, investments in the ongoing Lease & Operate projects under construction and the 2016 dividend payment. Cash and cash equivalent balances came in at US$1,039 million and committed, undrawn, long-term bank facilities stood at US$1,082 million. The average cost of debt stood at 4.5%, compared to 4.0% at the end of 2015.

Total equity as of June 30, 2016 decreased slightly to US$3,372 million versus December 31, 2015 under the negative impact of the mark to market revaluation of financial derivatives due to lower interest rates. The Company’s net debt to total equity ratio remained stable at 150% at year-end 2015 compared to 155% at the end of the first half of 2016.

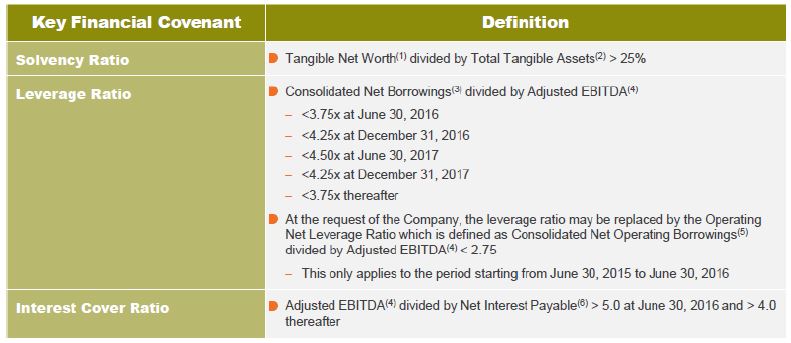

The Company’s solvency ratio stood at 32.7% while the leverage ratio came at 3.6x and the interest cover ratio came in at 6.9x, all firmly within covenant requirements.

The Company, together with its core relationship banks, signed an amendment to its Revolving Credit Facility (RCF) on April 18, 2016 providing headroom improvements to the leverage and interest coverage ratios. The agreed upon amendments, combined with a strong cash position, provide the Company with a larger degree of flexibility given the current industry downturn.

Including cash outflows for finance leases under construction previously reported as investing activities, cash from operating activities was positive US$166 million for the period compared to negative US$394 million during the first half of 2015. Cash outflows in finance leases under construction for the first half of 2016 decreased significantly to US$51 million compared to US$394 million in the year-ago period taking into consideration the strong decreasing investments in the fully consolidated FPSOs Cidade de Maricá, Cidade de Saquarema, Cidade de Ilhabela and Turritella.

Directional1 capital expenditure through the first half of 2016 amounted to a combined total of US$25 million, reflecting the advanced construction progress of the Company’s main projects which are expected to be completed over the next twelve months. These amounts correspond to the SBM Offshore share in SBM Inc. (the Company’s construction subsidiary) costs as well as costs directly incurred at the joint venture level.