Solid Results, Major New Order Won, Investing in Industry Leading Competitiveness

SBM Offshore is pleased to report revenues and EBITDA in line with management expectations. Lease and Operate delivered solid performance after successfully integrating three new large Floating Production, Storage and Offloading vessels (FPSOs) into the fleet. Turnkey performed well in the final phase of delivering projects to our clients. The Company was awarded the FPSOLizacontract by ExxonMobil, the industry’s only major FPSO contract award of the past 18 months. SBM Offshore committed to its standardization program Fast4WardTMby signing a new-build hull contract with China Shipbuilding Trading Company, Ltd. (“CSTC”) and the shipyard of Shanghai Waigaoqiao Shipbuilding and Offshore Co., Ltd. (“SWS”). Post-period, the purchase option on FPSOTurritellawas exercised by Shell and Heads of Terms for settlement were agreed with a majority group of primary layer insurers on SBM Offshore’s Yme insurance claim.

Break-even prices of deep water projects have substantially improved as result of cost deflation, more fit-for-purpose scope and leaner concept designs. In particular, deep water projects in areas with world class reservoirs have gained competitiveness against other oil and gas investment options. SBM Offshore is well positioned to benefit from this development. Whilst final investment decisions are on the increase, clients remain cautious and selective. As a result, the offshore services industry is gradually recovering but with a structurally lower activity level when compared to the market over the past decade.

Bruno Chabas, CEO of SBM Offshore, commented:

“SBM Offshore produced solid results for the first half of 2017, not only driven by the Lease and Operate segment, but also by sound performance in closing out Turnkey projects. With the three additional FPSOs ramping up, our fleet produced repeatedly more than 1 million barrels per day, which represents more than 10% of global deep water oil production. In today’s oil price environment, characterized by continued low prices, deep water field developments need to build on the competitiveness gained.

In an industry that more than ever needs performance, SBM Offshore brings competitive edge with its track record of reliable delivery and increased productivity through product standardization and faster times to market. Having delivered 34 FPSOs plus 300 years cumulative experience in operating its lease fleet, SBM Offshore is capitalizing on this experience through its Fast4WardTMprogram. The program’s result is an optimized design with standard specifications which leads to lower cost, higher quality and productivity on a de-risked plan with reduced safety exposure. Fast4WardTMaccelerates first oil by up to 12 months. SBM Offshore has now ordered its first standard new-build, multi-purpose hull. As our teams continue to demonstrate today, SBM Offshore is leveraging its experience in order to gain competitiveness and bring value to our clients by helping to lower break-even prices even further.”

Highlights

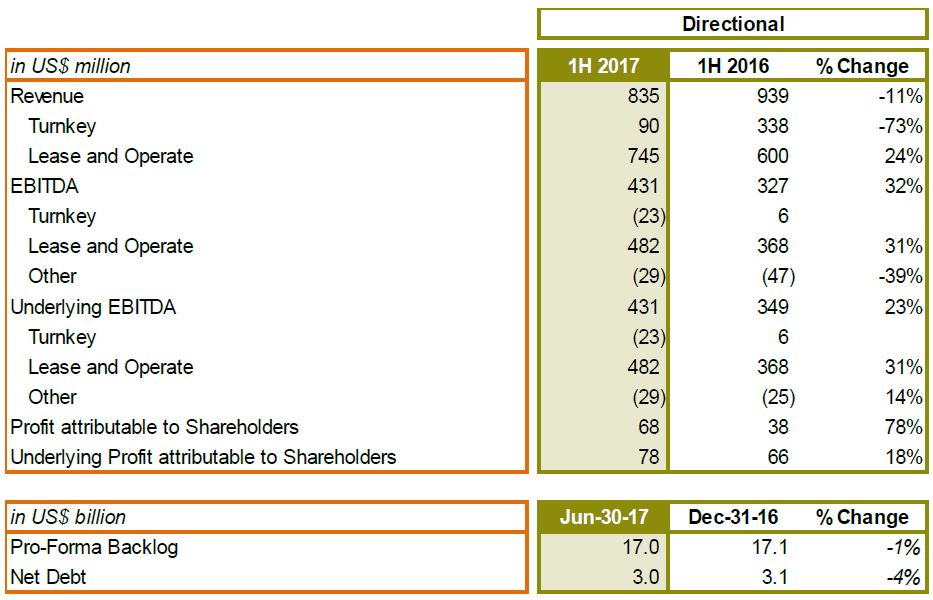

- Underlying[1]Directional[2]EBITDA increased by US$82 million, or 23%, to US$431 million, compared to the same period last year

- Underlying Directional EPS of US$0.39 per share, which represents an increase of 26% compared to first half of 2016

- Directional revenue of US$835 million, a decrease of 11% compared to same period last year

- Directional net debt at the end of June of US$3.0 billion, compared to US$3.1 billion at year-end 2016

- Confirmed award of FPSOLizacontracts by ExxonMobil, covering a lease period of 10 years; keeping backlog stable

- Sale of FPSOTurritellawith expected closing date in early 2018

- Settlement of Yme insurance claim agreed with majority group of primary layer insurers

- First new-build, multi-purpose FPSO hull under SBM Offshore’s Fast4WardTMprogram on order

- Expanded Directional reporting with introduction of Directional balance sheet and cash flow statement

- 2017 guidance for Directional revenue reiterated at “around US$1.7 billion” and for Underlying Directional EBITDA updated to “above US$750 million”

Overview

Underlying EBITDA 1H16 excludes US$22 million compliance provision, Underlying Profit additionally excludes US$6 million for 1H16 and US$11 million for 1H17 relating to the increase of the net present value of the future payments (instalments and bonus reductions) related to compliance provision.

Directional revenue decreased by 11% to US$835 million, due to lower activity in Turnkey caused by a reduction in order intake as a result of continued difficult market conditions, offset by a 24% increase in revenues in Lease and Operate driven by the three FPSOsCidade de Maricá,Cidade de SaquaremaandTurritellaadded to the fleet during 2016 which have now contributed in full during the first half year.

Underlying Directional EBITDA increased by 23% to US$431 million, which was driven by a 31% or US$114 million increase in Lease and Operate to US$482 million, partially offset by a US$29 million decrease in Turnkey. The Turnkey contribution was limited to a negative EBITDA of US$23 million, mainly due to sound performance in project close out, releasing project contingencies. The underlying factor contributing to this negative EBITDA is the Company’s stated strategy of investing in retaining necessary capacity and protecting its experience and know-how for the future.

Period Review

FPSOLiza

At the end of last year, SBM Offshore commenced the Front-End Engineering and Design (FEED) and early Engineering, Procurement and Construction (EPC) work scope for the FPSOLiza. After the announcement of June 22, 2017 of the award of the FPSOLizacontracts, the Company has started the EPC phase. This work is progressing well in close cooperation with the client team, benefiting from seamless project phasing, connecting early design to EPC scope of this fast-track project.

Turrets & Mooring Systems

SBM Offshore’s major turret projects Prelude and Ichtys have entered the offshore commissioning phase, and continue to progress in accordance with clients’ schedules and contractual planning.

Fast4WardTM

SBM Offshore has reached an important milestone in its Fast4WardTMprogram. This program can make our clients’ deep water project returns more attractive in today’s oil price environment. Oil developments are increasingly in deeper water with harsher conditions, requiring heavier installations on deck, despite space and weight constraints. Deep water projects are required to be more efficient and reliable, faster, safer with lower project break-even prices. Fast4WardTMaddresses these industry challenges through optimized design and standard specifications. The program capitalizes on what SBM Offshore has learned from its 118 Turnkey product deliveries, including 34 increasingly complex deep water FPSOs, as well as from its long history of operating one of the world’s largest FPSO fleets.

Fast4WardTMbrings client benefits on two levels. First, the standardization of installations releases all the benefits to be had from a topsides catalogue. This topsides catalogue is now available to be used on existing tenders, including VLCC (Very Large Crude Carrier) conversions and increasingly incorporates processes that have traditionally been considered too difficult to standardize. Second, the program allows for the use of a standard, multi-purpose, new-build hull. Using such a hull, Fast4WardTMcan accelerate delivery of an FPSO by up to 12 months. For a typical project, this can boost value for a client by more than US$0.5 billion, materially lowering project break-even prices. Through standardization and repetition SBM Offshore can now offer greater safety, more cost efficiency and productivity, more reliability and more assured delivery deadlines.

In June 2017, the contract for the first new-build, multi-purpose hull was signed with CSTC and SWS, a global leader in ship building, and so now the EPC phase of the Fast4WardTMhull has started. Capital commitments are phased over time, with planned yard expenditure of c. US$20 million in 2017 and c. US$55 million in 2018, subject to delivery of agreed milestones. SBM Offshore believes that Fast4WardTMis the answer to today’s industry challenges and has identified appropriate deep water development opportunities that it is targeting for the deployment of the hull and the associated topsides catalogue for the benefit of clients.

Operational Update

The Lease and Operate fleet uptime performance year-to-date was 98.1%. This operational uptime shows a significant improvement compared to uptime of 96.8% for the year 2016.

Regarding the Company’s year-to-date safety performance, Reported Total Recordable Injury Frequency Rate (TRIFR) was 0.24, a marked improvement compared to last year. SBM Offshore continues to invest in its HSSE culture and processes to support its ambition for an industry leading performance.

Post-period events

FPSOTurritella

The FPSOTurritellasale announced on July 11, 2017, represents a post-period, non-adjusting event. As such, the mid-year financials are not impacted by this transaction. The precise financial impacts are dependent on the timing of the transaction which has yet to be finally determined but is currently expected in early 2018. The income statement will reflect: i) the difference between the proceeds from disposal and the carrying amount of the asset (being the net book value of Property, Plant and Equipment under Directional and the net investment in the lease reported as a Finance Lease Receivable under IFRS); ii) costs related to the transaction, including settlement arrangements with joint venture partners; and iii) the impact of the unwinding of the interest rate swap and amortization of the upfront transaction costs related to the project loan to be repaid.

For the purposes of guidance, assuming a closing date in early 2018, the total impact of the above on the Company’s net result is expected to be a gain of c. US$120 million under Directional reporting. Under IFRS, as profits are front-end loaded from the inception of a finance lease ahead of the cash flow, the transaction is expected to result in a loss of c. US$130 million. These results reflect for the most part partner settlement arrangements, but also include the effects of the unwinding of hedging instruments and unamortized transaction costs. Under IFRS, there is also an impact from the fact that the amount to be received from the client, on exercising the option to purchase, is 4% less than the remaining net investment in the lease. The aggregate of previously booked profits related to the Turritella project combined with the impact from the transaction will be identical under both Directional and Group Result IFRS, with profit recognition to date having been accelerated under IFRS. At the transaction date, SBM Offshore expects to receive c. US$540 million cash, which will be used for unwinding of partner commitments, hedging instruments and repayment of the project loan. The transaction is expected to decrease Directional net debt by c. US$450 million.

Yme insurance claim

The Heads of Terms for a settlement agreement with a majority group of primary layer insurers relating to SBM Offshore’s Yme insurance claim is also a post-period, non-adjusting event. From this settlement, SBM Offshore expects to receive net cash proceeds exceeding US$100 million. The final agreement remains subject to contract. SBM Offshore continues to pursue its claim against all remaining insurers, the trial of which is scheduled to commence October 2018.

FPSOMarlim Sulwhich was decommissioned in April 2016, was sold and transferred off balance sheet in July 2017 for recycling, in-line with SBM Offshore policies and in accordance with the Hong Kong convention.

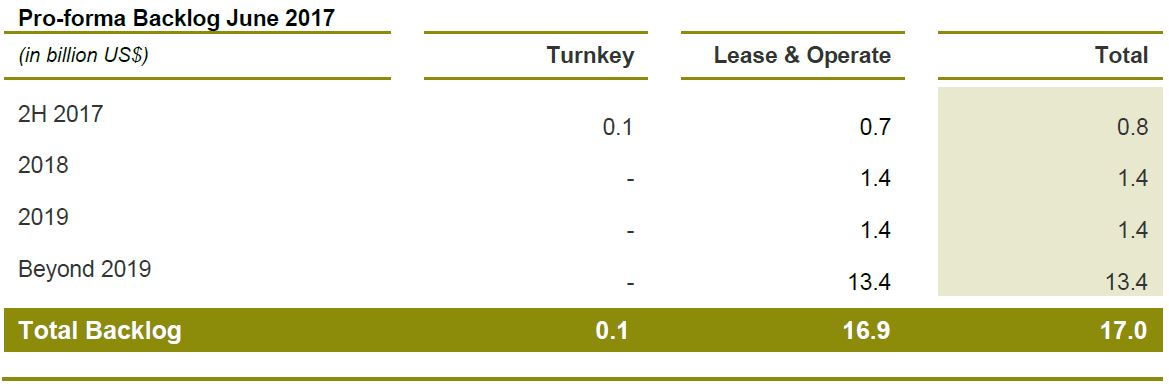

Directional Backlog

For this period, SBM Offshore provides a pro-forma Directional backlog overview, which provides a normalized outlook on existing leases.

Normally, the backlog would not yet take the sale of FPSOTurritellainto account, pending signature of the sales contract, or the agreed FPSOLizaoperating and maintenance scope, which is pending a final work order. However, for the purposes of the pro-forma backlog represented in the table below, both have been taken into account.

The pro-forma Directional backlog remains nearly constant at US$17.0 billion compared to year-end 2016, despite the turnover booked of US$835 million during the first half of 2017. Order intake for the first half year includes the FPSOLizaaward and the 5-year operating and maintenance contract on FPSOSerpentina. This increase is partially offset by the decrease in backlog resulting from the sale of FPSOTurritella, effective early 2018.

Directional results

Since 2013, SBM Offshore has been disclosing its Directional income statement in order to provide more transparency on underlying business performance and cash flow generation. The Company is extending this disclosure to include a Directional balance sheet and cash flow statement in the presentation accompanying the mid-year 2017 results announcement. Going forward, with effect from full-year 2017 reporting, SBM Offshore will incorporate the Directional balance sheet and cash flow statement in the Consolidated Financial Statements.

Directional reporting remains tied to IFRS reporting, but in two defined instances chooses alternative, but IFRS defined, accounting treatments, consistently applied. First, on consolidation, where IFRS provides for equity and full consolidation for joint-ventures owning lease and operate contracts, Directional makes use of the proportionate accounting method. This does not affect equity accounted joint-ventures owning yards and installation vessels, which remain equity accounted under Directional. Second, in deciding which lease treatment to use, Directional accounting treats all leases as operating leases. These changes are designed to bring Directional accounting more in line with the cash that has actually been generated, but yet keep Directional reporting anchored to well-defined IFRS principles. This approach also facilitates straightforward reconciliation of Directional reporting to IFRS and Directional reporting being fully auditable by the Company’s external auditors.

Funding and Directional net debt

At the end of June 2017, SBM Offshore had Directional cash and undrawn committed credit facilities totaling US$1,752 million compared to US$1,823 million at year-end 2016. Strong Directional cash flow from operations driven by Lease & Operate was used to decrease payables, mainly related to Turnkey, purchase a vessel to support bidding activity, pay interest, redeem project debt, pay the dividend over 2016. Directional net debt decreased from US$3.1 billion at year-end 2016 to US$3.0 billion at the end of June 2017.

Compliance

Discussions with the Brazilian authorities and Petrobras regarding the Leniency Agreement signed on July 16, 2016 that was subsequently sent back to the Public Prosecutor by the Brazilian Fifth Chamber for Coordination and Review and Anti-corruption for adjustments, are ongoing. Any adjusted Leniency Agreement signed with the Public Prosecutor’s Office (“MPF”) will again be subject to approval by the Fifth Chamber whereas an adjusted Leniency Agreement signed with the Brazilian Ministry of Transparency, Oversight and Control (“MTFC”), would remain subject to review by the Federal Court of Accounts Tribunal de Contas da União, (“TCU”).

In the United States, discussions with the Department of Justice (“DOJ”) are advancing. These regard the investigation the DOJ had closed in November 2014 and reopened early in 2016 and its inquiry into Unaoil, a company that SBM Offshore had engaged as an agent prior to 2012 in relation to delivery of barges, offshore terminals and maintenance.

Pending the discussions with the Brazilian authorities and the DOJ, the Company cannot provide further clarity or assurance on the outcomes of these discussions, or on the timing thereof.

Outlook and Guidance

As expected, the industry is witnessing a gradual recovery. Although significant decreases in project break-even prices are making deep water more competitive, our clients remain cash constrained and selective in making investment decisions. Medium to long term, the Company believes that deep water offshore will regain a solid position in the future energy supply.

The Company is reiterating 2017 Directional revenue guidance of around US$1.7 billion, with around US$1.5 billion from Lease and Operate and around US$200 million from Turnkey.

Full-year 2017 Directional Underlying EBITDA guidance is updated from “around US$750 million” to “above US$750 million”. This does not include the non-recurring positive effect from the agreed Heads of Terms relating to SBM Offshore’s Yme insurance case, nor does it include any effects from the completion of the Turritella transaction planned for early 2018.

FINANCIAL REVIEW

DirectionalPerformance

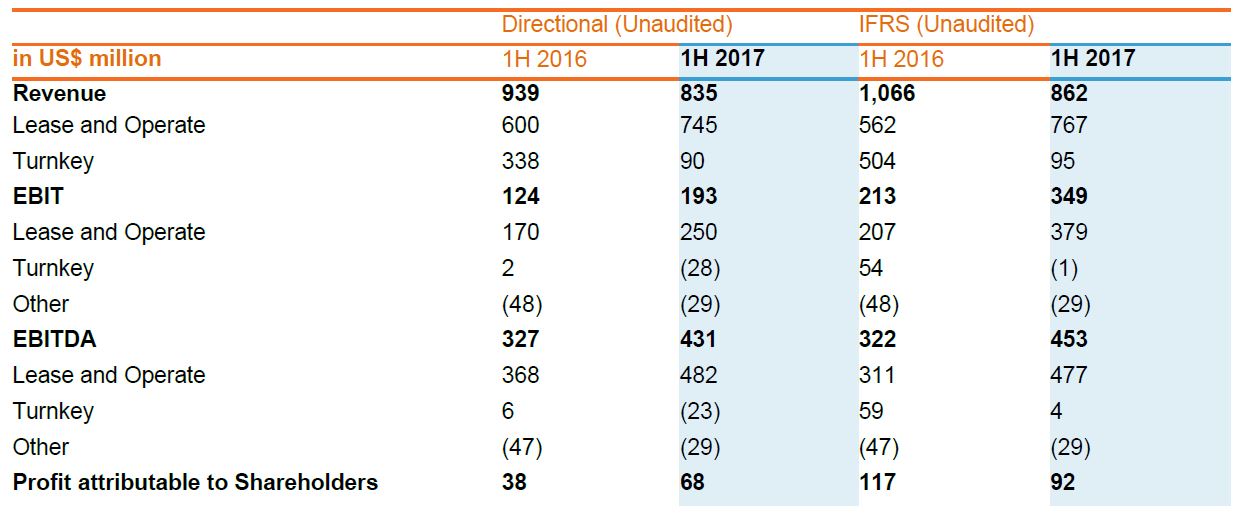

Directional revenue decreased by 11% to US$835 million compared to US$939 million in the year ago period reflecting the finalization of major turnkey projects in 2016 and lack of significant order intake over the prior periods. This was not fully offset by increased revenue from the start-up of the completed vessels in the lease and operate segment. Directional revenue by segment was as follows:

- Directional Lease and Operate revenue increased by 24% to US$745 million, representing 89% of total Directional revenue over the first half year of 2017, up from the 64% contribution in the year-ago The increase in segment revenue is attributable to the start-up of FPSOsCidade de Maricáin February 2016 andCidade de SaquaremaandTurritelladuring the second half of 2016, while no vessel has been decommissioned since the year-ago period.

- Third-party Directional Turnkey revenue came down 73% year-on-year to US$90 million, representing only 11% of total first half 2017 This compares to US$338 million or 36% of total revenue, in the year- ago period. The decrease is mostly attributable to the completion stage reached in the course of 2016 on the FPSOsCidade de Maricá,Cidade de SaquaremaandTurritella, the decrease of offshore services activities as well as the low order intake in 2014, 2015 and 2016 as a result of the market downturn.

Directional Earnings Before Interest, Taxes Depreciation and Amortization (EBITDA) for the first half year of 2017 was US$431 million, an increase of 32% compared to the EBITDA of US$327 million in the year-ago period. This variance was primarily thanks to:

- An increase in Directional Lease and Operate EBITDA from US$368 million in the year-ago period to US$482 million in the first half year of 2017 driven by the full half-year contribution of the three FPSOs that came into production during First half year 2017 Directional Lease & Operate EBITDA margin came in at 65% compared to 61% during the first half year of 2016, also reflecting the positive contribution of the three FPSOs joining the fleet.

- Directional Turnkey EBITDA decreased by US$29 million due to the decline of Turnkey activity year-on- year, mitigated by positive close outs on projects finalization, under-recovery monitoring, significant saving on Turnkey overheads and the one-off nature of restructuring costs in Directional Turnkey gross margin expressed as percentage of Turnkey revenue came in at 28%, almost stable compared to 29% in the previous period.

- A reduction of US$18 million in other non-allocated costs charged to EBITDA driven principally by the update of the provision for contemplated settlement with Brazilian authorities and Petrobras booked on the first half of 2016 for US$22

For the first half-year of 2017, Directional EBIT increased to US$193 million, compared to US$124 million in 2016. EBIT variations per segment are the same as for the EBITDA, the increase of Lease and Operate EBITDA (US$114 million) being however partially offset by an increase of depreciation charges (US$35 million) related to the three new FPSOs that came into production in 2016.

Directional net financing costs totalled US$112 million in the first half of 2017, up from US$86 million in the year-ago period. The increase was primarily due to the full half-year impact of interest costs related to the project financing of the three vessels that came into operation during 2016.

The effective tax rate is stable year-on-year with an effective tax rate of 6.5% over the first half year of 2017, compared to 7% in the year-ago period.

The Company recorded a Directional consolidated net income of US$68 million, or US$0.33 per share, for the first half year of 2017, up from US$38 million, or US$0.18 per share, in the year-ago period.

IFRS Performance

Reported first half–year 2017 IFRS revenue decreased by 19% to US$862 million versus US$1,066 million in the first half year of 2016. The decrease is driven by the slowdown of Turnkey construction and offshore services activities despite a 36% year-on-year increase of revenue in the Lease and Operate segment.

IFRS EBITDA amounted to US$453 million, representing a 40% increase driven by the Lease and Operate segment compared to US$322 million in the year-ago period.

IFRS EBIT increased to US$349 million, representing a 64% increase compared to US$213 million in 2016.

IFRS net income attributable to shareholders for the first half year of 2017 came in at US$92 million compared to US$117 million for the year-ago period.

IFRS Statement of Financial Position

Total assets under IFRS decreased by US$0.3 billion to US$11.2 billion as of June 30, 2017 compared to US$11.5 billion at year-end 2016. This decrease reflects the regular periodic unwinding of finance lease receivables, regular depreciation on fixed assets and a lower cash position.

IFRS Shareholder’s equity increased from US$2,516 million at year end 2016 to US$2,641 million at June 30, 2017 mostly thanks to the positive net result over the first half-year of 2017 and a significant increase in the fair value of forward currency contracts as a result of the currency appreciation of hedged currencies against the US$, partially offset by the dividend paid over 2016.

IFRS net debt decreased by US$191 million to US$5,025 million at June 30, 2017, coming down from US$5,216 million at year end 2016. The decrease in net debt is as a result of strong operating cash-flow generation, partially offset by increased net financing cost and payment of the 2016 cash dividend. Cash and cash equivalent balances came in at US$824 million at June 30, 2017 compared to US$904 million at December 31, 2016 while total loans and borrowings came down from US$6,120 million at year end 2016 to US$5,849 million.

IFRS cash from operating activities for the period was positive US$396 million compared to US$166 million during the first half of 2016. This primary reflects the cash generated by the three new FPSOs that came into production in 2016.

The relevant banking covenants (Solvency, Net Debt/Adjusted EBITDA, Interest Cover) were all met at June 30, 2017. As in previous years, the Company has no off-balance sheet financing.

Further financial information is provided in the Condensed Consolidated Interim Financial Statements.

Analyst Presentation & Conference Call

SBM Offshore has scheduled a conference call and webcast of its presentation to the financial community followed by a Q&A session at 10.00 Central European Time on Wednesday, August 9, 2017.

The presentation will be hosted by Bruno Chabas (CEO), Philippe Barril (COO), Erik Lagendijk (CGCO) and Douglas Wood (CFO). Interested parties are invited to listen to the call by dialing +31 20 531 5851 in the Netherlands, +44 203 365 3210 in the UK or +1 (866) 349 6093 in the US. Interested parties may also listen to the presentation via webcast through a link posted on the Investor Relations section of the Company’s website.

The live webcast and replay, which should be available shortly after the call, will be available at:https://ssl.webinar.nl/webcast/sbmoffshoreinvestors/20170809_1

| FinancialCalendar | Date | Year |

| Trading Update 3Q 2017 – Press Release | November 8 | 2017 |

| Full-Year 2017 Earnings – Press Release | February 8 | 2018 |

| Annual General Meeting of Shareholders | April 11 | 2018 |

| Trading Update 1Q 2018 – Press Release | May 10 | 2018 |

| Half-Year 2018 Earnings – Press Release | August 9 | 2018 |

| Trading Update 3Q 2018 – Press Release | November 15 | 2018 |

Note: dates in bold have changed as communicated in SBM Offshore’s press release dated 10 July 2017

Corporate Profile

SBM Offshore N.V. is a listed holding company that is headquartered in Amsterdam. It holds direct and indirect interests in other companies that collectively with SBM Offshore N.V. form the SBM Offshore group (“the Company”).

SBM Offshore provides floating production solutions to the offshore energy industry, over the full product life-cycle. The Company is market leading in leased floating production systems with multiple units currently in operation and has unrivalled operational experience in this field. The Company’s main activities are the design, supply, installation, operation and the life extension of Floating Production, Storage and Offloading (FPSO) vessels. These are either owned and operated by SBM Offshore and leased to its clients or supplied on a turnkey sale basis.

As of December 31, 2016, Group companies employ approximately 4,750 people worldwide. Full time company employees totaling c. 4,250 are spread over five regional centers, ten operational shore bases and the offshore fleet of vessels. A further 500 are working for the joint ventures with several construction yards. For further information, please visit our websiteat www.sbmoffshore.com.

The companies in which SBM Offshore N.V. directly and indirectly owns investments are separate entities. In this communication “SBM Offshore” is sometimes used for convenience where references are made to SBM Offshore N.V. and its subsidiaries in general, or where no useful purpose is served by identifying the particular company or companies.

The Management Board

Amsterdam, the Netherlands, August 9, 2017

For further information, please contact:

InvestorRelations

Bert-Jaap Dijkstra

Investor Relations Director

| Mobile NL:

Mobile MC:

|

+31 (0) 6 2114 1017

+33 (0) 6 4391 9302

|

| Telephone: | +377 9205 1732 |

| E-mail: | Bert-Jaap Dijkstra |

| Website: | www.sbmoffshore.com |

Media Relations

Vincent Kempkes

Group Communications Director

| Telephone: | +31 (0) 20 2363 170 |

| Mobile: | +31 (0) 6 25 68 71 67 |

| E-mail: | Vincent Kempkes |

| Website: | www.sbmoffshore.com |

Disclaimer

This press release contains inside information within the meaning of Article 7(1) of the EU Market Abuse Regulation. This press release contains regulated information within the meaning of the Dutch Financial Markets Supervision Act (Wet op het financieel toezicht). Some of the statements contained in this release that are not historical facts are statements of future expectations and other forward-looking statements based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those in such statements. Such forward-looking statements are subject to various risks and uncertainties, which may cause actual results and performance of the Company’s business to differ materially and adversely from the forward-looking statements. Certain such forward-looking statements can be identified by the use of forward- looking terminology such as “believes”, “may”, “will”, “should”, “would be”, “expects” or “anticipates” or similar expressions, or the negative thereof, or other variations thereof, or comparable terminology, or by discussions of strategy, plans, or intentions. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described in this release as anticipated, believed, or expected. SBM Offshore NV does not intend, and does not assume