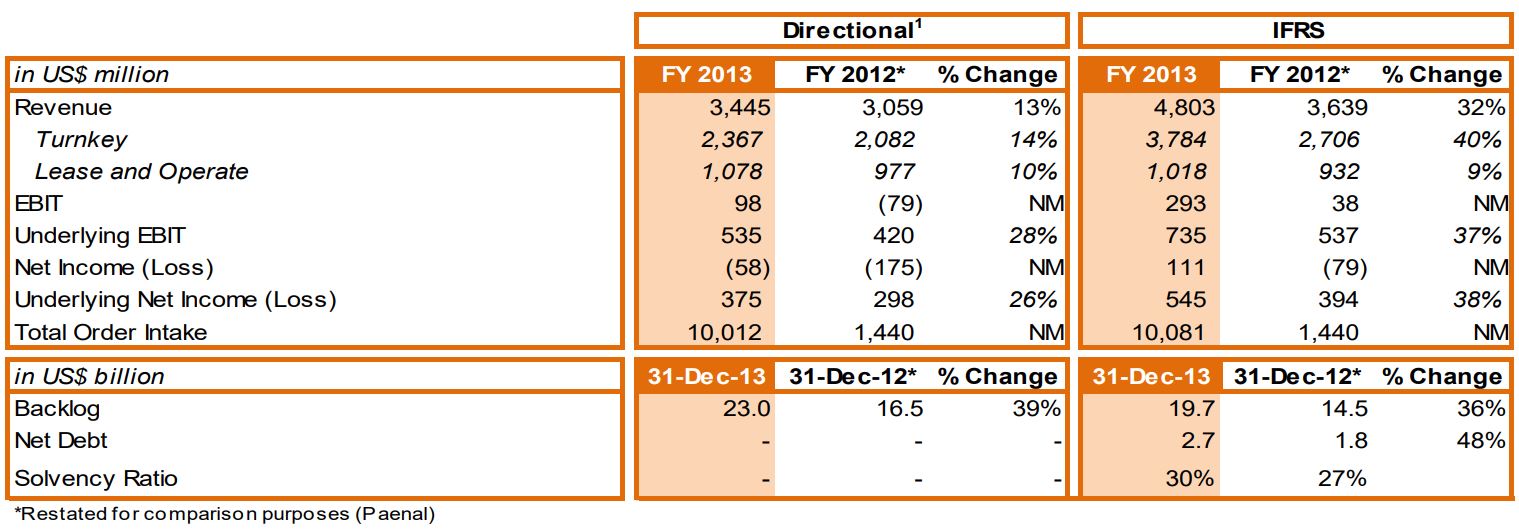

SBM Offshore finished 2013 with a strong underlying financial performance, ahead of expectations. The Company has now put most of its legacy projects to rest, secured the balance sheet and refocused its activity around the FPSO-led strategy. Directional1 revenue increased 13% to US$3,445 million, while Directional1 backlog reached US$23 billion. This was reinforced by strong operational performance with consistently high uptime across the fleet of over 99%.

Three prestigious FPSO awards were won during the year (Cidade de Maricá, Cidade de Saquarema and FPSO Stones), two FPSOs (Cidade de Paraty and OSX-2) were delivered on time and on budget and Deep Panuke platform reached full production capacity and is now fully on hire.

Bruno Chabas, CEO of SBM Offshore commented:

“2013 was a year of progress on all fronts: strategic, operational and financial. Our Company is now focused, without distraction, on its future. Our outstanding project wins in Brazil and the US Gulf of Mexico sum-up what is best about SBM Offshore: staying close to our clients, using our technological edge to solve their problems and taking pride in our work. Our industry faces a challenging period, but we believe SBM Offshore is strongly positioned. We possess a balanced portfolio of projects, the ability to offer a choice of financing options for clients and the leading position in a niche service which the oil industry needs to sustain future production.”

Financial Highlights

•

Directional1 revenues were up 13% to US$3,445 million in FY‟13, and underlying Directional1 EBIT increased by 28% to US$535 million

•

Directional1 Backlog up by 39% to a record level of US$23 billion

•

Awarded three Lease & Operate FPSO contracts: Cidade de Maricá, Cidade de Saquarema and FPSO Stones.

•

FPSOs Cidade de Paraty and OSX-2 delivered on time and on budget

•

Cash at the end of the period was US$200 million; undrawn credit facilities of US$1,234 million

•

Net debt at the end of December stood at US$2,691 million

•

Agreement to decommission the Yme platform and settle outstanding issues with Talisman for US$470 million

•

Update to residual values and decommissioning costs resulted in one off non-cash charges of US$158 million

•

Successful 10% Rights Issue at €10.07 per share raised US$247 million in new equity

Guidance

Management is issuing 2014 Directional1 revenue guidance at similar levels to 2013, of approximately US$3.4 billion, which is based on conservative award assumptions. Turnkey and Lease & Operate revenues are also expected to be approximately in line with 2013 levels.

2013

Company Overview

Introduction

The Company began its transformation in 2012, re-focusing its strategy around FPSOs and related products and services, followed by far reaching changes to the organisational structure emphasising accountability, transparency and compliance. The results, strong revenue growth, good core performance and record backlog clearly began to emerge in 2013. The transformation continues as the Company focuses on strengthening project controls, support functions and operational disciplines across the business. This is being achieved through a programme to improve ways of working for people, and through processes and systems designed to increase effectiveness, deliver control and allow the Company to “work as one.”

Apart from the on-going internal investigation into potentially improper sales practices, the Company has largely consigned its legacy issues to the past. The Yme settlement was signed in March and the Deep Panuke platform achieved Production Acceptance in December 2013. Asset values have been adjusted where required. Through the corporate and project financing activities completed in the year, the financial position of the Company is markedly strengthened enabling it to competitively address the increasing demand for larger and more complex projects from our clients.

The project award delays encountered in 2012, combined with a strong commercial effort, resulted in record order levels in 2013 with Directional1 Order Intake of US$10.0 billion and Directional1 Backlog of US$23.0 billion.

Consistent with the Company‟s strategy to focus on its core business and to further strengthen the financial position, a number of non-core asset divestments were made during the period, which include the sale and lease back transactions of two out of three office properties in Monaco and the sale of its non-core “COOL™ hose” technology.

In the first half of the year, the Company strengthened its financial position through a 1 for 10 rights offering of new ordinary shares raising US$247 million and, as a result of the settlement with Talisman, an additional US$27 million top-up from HAL Investments B.V. (HAL) as a share premium contribution on the new ordinary shares it acquired through a private placement in December 2012.

The Company secured a Project Loan facility for FPSO N’Goma for US$600 million and bilateral credit facilities for FPSO Cidade de Maricá and Cidade de Saquarema for US$600 million. The additional liquidity and greater financial flexibility have further improved the Company‟s risk profile for securing funding for future projects.

Directional1 Reporting

In 2013, in order to provide its shareholders with clarity on business performance above and beyond the regular IFRSbased disclosures, the Company introduced Directional1 reporting. Directional1 reporting addresses the complexity in the Group‟s business model whereby turnkey sales are combined with construction projects for its own lease & operate portfolio. Furthermore, the Company‟s FPSO lease & operate contracts are increasingly classified as „finance leases‟, which adds further complexity by accelerating revenue and profit recognition into the construction phase, well before rents are invoiced to, and paid by, the client. The Directional1 view extends reporting with non-IFRS disclosures showing revenues and results more in line with operating cash flows to simplify some of these complexities. This is designed to increase transparency and understanding of performance and provide disclosures of Backlog and Income Statement based on Directional1 principles.

Directional1 reporting principles are:

•

Directional1 reporting is an additional disclosure to IFRS reporting

•

Directional1 reporting assumes all lease contracts are classified as operating lease

•

Directional1 reporting is limited to restating revenue and operating income; no balance sheet restatements are made

•

Directional1 reporting is included in the Financial Review

In order to introduce Directional1 reporting, the Company achieved the following steps:

•

Disclosure of Directional1 income statement and Backlog for H1 2013 and the H1 2012 comparison was made in August with the Half-Year results

•

2013 transition period to promote Directional1 reporting as the main indicator for Company performance and variance analysis

•

Full Year 2013 Directional1 income statement disclosed with 2012 comparison

•

2014 guidance for Directional1 revenue

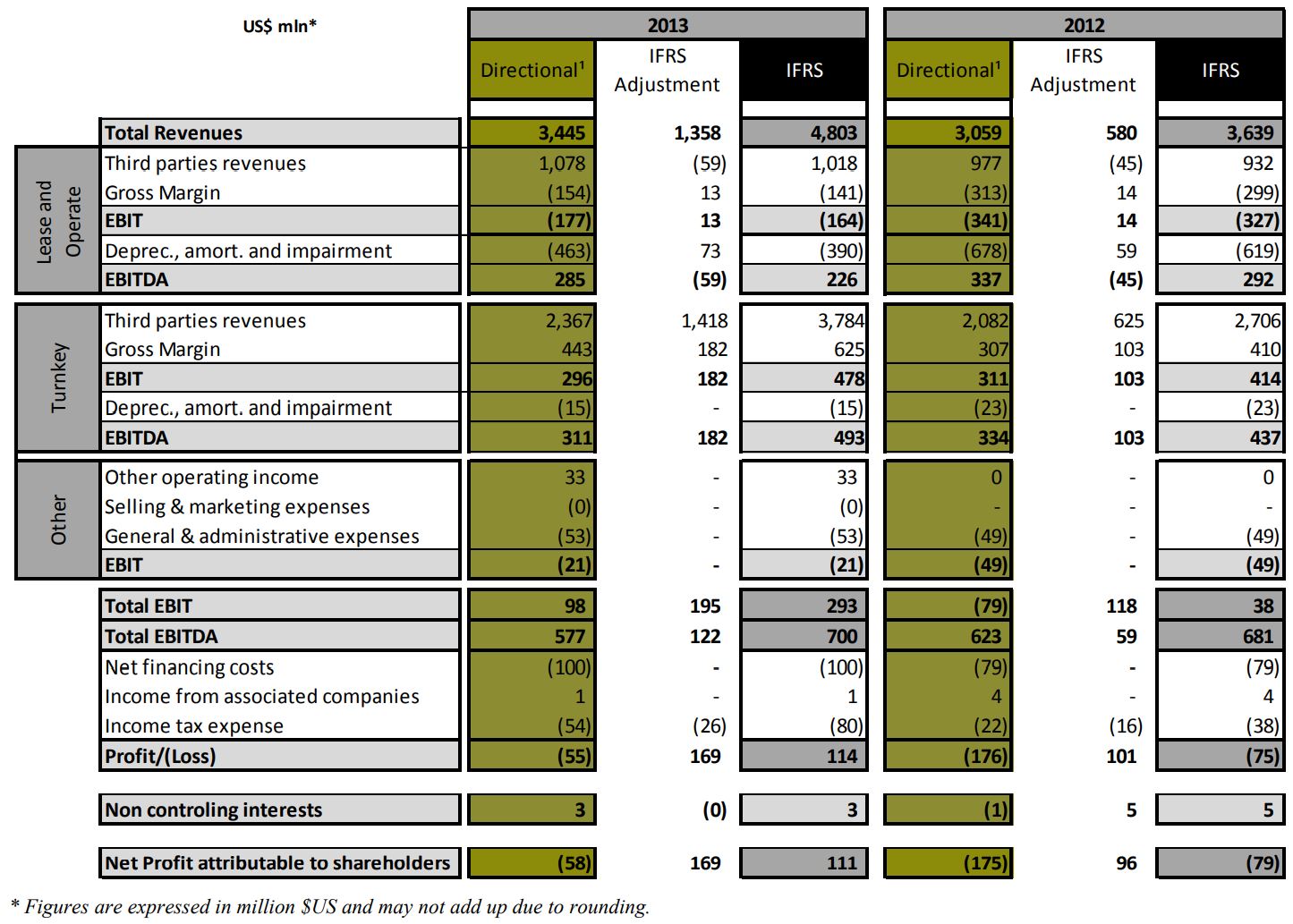

The need for the introduction of Directional1 reporting is acute and significant: revenue reported under IFRS rules exceeds the Directional1 view by some US$1.4 billion in 2013. This represents the present value of future income to be invoiced and realised over the next 20 years. Under IFRS the Company reports a US$111 million positive net income attributable to shareholders for 2013, while the Directional1 view shows a loss of US$58 million. The Management Board highlights these fundamental and significant differences to allow investors a balanced understanding of the results, giving insight in both rules and reality.

HSSE

Over the course of 2013 the Company achieved a good safety performance in a range of its business activities, and similar to that of 2012 with a Total Recordable Injury Frequency Rate (TRIFR) of 0.40 in 2013 compared to 0.38 in 2012. However, the Lost Time Injury Frequency Rate (LTIFR) deteriorated to 0.15 in 2013 from 0.06 from 2012. A number of corrective actions have been taken to help raise our standards.

Compliance

In 2012, the Company announced it had initiated an internal investigation, conducted by outside counsel and forensic accountants, into potentially improper sales practices. The Company has disclosed the results of the internal investigation to the appropriate authorities and remains in active dialogue. As the investigation is still in progress it is not possible to provide further information or an estimate of the outcome, financial or otherwise. The Company has continued and expanded its efforts, started in 2012, to enhance its compliance program.

Yme

In March, the Company reached an agreement with Talisman to terminate the Yme MOPUstor contract for a settlement of US$470 million. The settlement included the termination of the existing agreements and arbitration procedures and the decommissioning of the MOPU. As the Company had already made a provision of US$200 million in 2012, the difference of US$270 million was recognised in the 2013 results.

Deep Panuke

The Company completed the debottlenecking process, and brought the Deep Panuke platform to full production capacity safely and received a Production Acceptance Notice (PAN) from the client in December 2013. The platform is currently on hire and generating full day rate.

Strategy

Last year the Company re-focused its strategy on its core business of FPSOs and associated products and services. Since the beginning of 2013, new award announcements for two FPSOs for Petrobras in Brazil and one FPSO for Shell in the Gulf of Mexico demonstrate progress is well underway. As the industry leader, the Company continues to strive for an improved risk/reward balance for its FPSO products and services and has identified an encouraging pipeline of projects in the medium term.

Investing in our Future

Over the course of 2013, the Management Board focused its attention on three core strands of activity to develop and improve SBM Offshore‟s future performance. During 2014, these programmes will carry incremental costs equivalent to 2.5%-3% of Directional1 revenue.

With the lengthening life spans of FPSOs, there is an emerging need for a defined fleet maintenance programme, over and above the standard operational expenditure on individual vessels. This will be a focused two year investment programme with clear operational and financial benefits.

Despite recent progress, there is a distinct need to permanently embed improved efficiency and ways of working across multiple disciplines. A two year transformation programme, named Odyssey 24, will create the foundation to deliver consistently outstanding performance. The programme is led by SBM senior staff members, dedicated for the project duration, and using external advisors.

Maintaining its technological lead position in complex floating production systems, and associated mooring systems, is critical for SBM Offshore. The company will continue to identify technology trends in the offshore oil & gas market, prioritising development work to address key areas of demand.

Outlook and Guidance 2014

2013 has been a strong year for SBM Offshore. Revenue growth and underlying EBIT margins were excellent as the Company successfully progressed its EPC and Lease & Operate portfolio.

The Company is providing 2014 guidance on the basis of Directional1 results. Directional1 revenue is expected to come in at similar levels as in 2013, approximately US$3.4 billion, which is based on conservative award assumptions. Turnkey and Lease & Operate revenues are also expected to be approximately in line with 2013 levels.

The Company expects a level of capital investments higher than 2013 levels. Furthermore, the Company will continue to attract necessary project financing for the funding of new, or recently awarded, leased FPSOs under construction.

Dividend

The Management Board reiterates that the Company will not pay a dividend over 2013, in view of the losses incurred in 2011 and 2012 and the need to strengthen the balance sheet. The Management Board intends to discuss at the Annual General Meeting (AGM) in 2015 a change of dividend policy, making dividends dependent on available free cash flow as opposed to the existing policy of paying out 50% of IFRS net income. Given the on-going execution of the Group‟s record project backlog, the Management Board does not exp