Revenue up 6%; Outlook confirmed

SBM Offshore’s execution of projects on hand in the first six months of the year led to better than expected revenue growth. The Company is making progress towards resolving its compliance issue, as evidenced by the US$240 million provision, secured US$1.45 billion of financing for Cidade de Maricá and signed the Operations & Maintenance contract for FPSO Turritella. Directional¹ Backlog stands at US$21.5 billion. SBM Offshore continued to achieve over 99% uptime across the fleet. The Company delivered the Kikeh brownfield extension project on time and on budget while also reaching a settlement of claims arising from the Deep Panuke project.

Bruno Chabas, CEO of SBM Offshore commented:

“In financial and operational terms, the first half of 2014 has been a period of solid performance. We have also made progress towards the closure of our final legacy issue with a provision against a potential settlement.

The period also presented a significant challenge: our withdrawal from two current tenders in Brazil pending the outcome of the compliance investigation. Nevertheless, the Company has built a decades-long track record of close cooperation with Petrobras. We believe this will provide a basis to resume a successful working relationship, once the investigation is properly completed.

Tendering activity remains high, and there is industry consensus on a substantial number of new FPSOs and turrets due for award in the coming years. Thus, while we remain cautious on the timing of individual awards in the short term, we have a sound basis for confidence in our medium and long term prospects.“

Financial Highlights

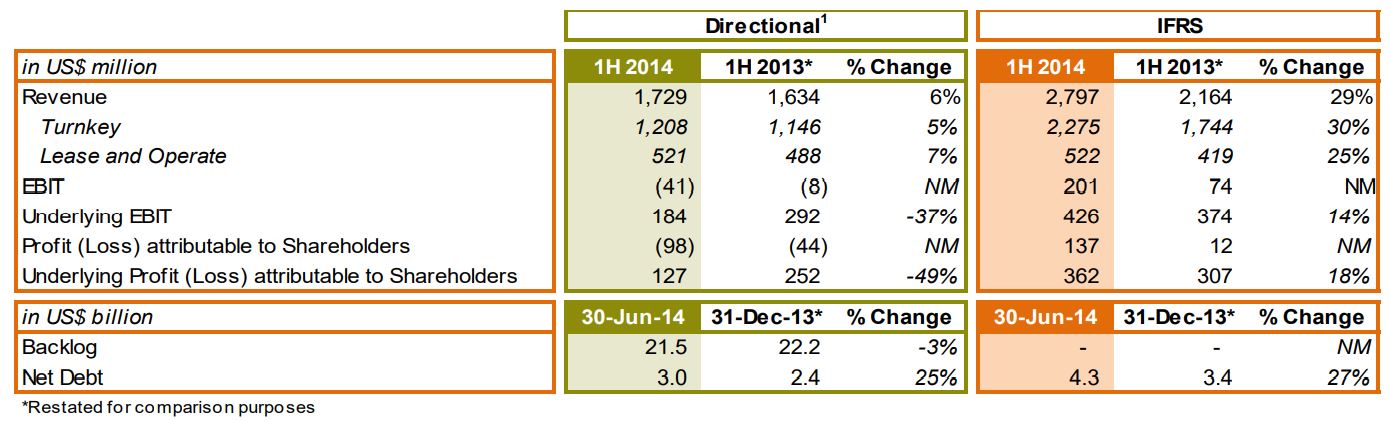

- Directional¹ revenue ahead of expectations at US$1,729 million

- Underlying Directional¹ EBIT decreased by 37% to US$184 million, compared to a strong 1H 2013

- Directional¹ Backlog stands at US$21.5 billion, including the O&M contract for the Shell FPSO Turritella

- Cash at the end of the period stood at US$154 million; undrawn credit facilities of US$939 million

- Net debt at the end of June stood at US$4,302 million, under new IFRS reporting standards

- Project financing secured for Cidade de Maricá totaling US$1.45 billion at an average cost of debt of 5.3% with 12 and 14 year maturity tranches

- US$240 million provision related to the compliance investigation

Guidance

Management is confidently reiterating 2014 Directional¹ revenue guidance of US$3.3 billion, of which US$2.3 billion is expected in the Turnkey segment and US$1.0 billion in the Lease & Operate segment.

First Half 2014 Results

Project Review

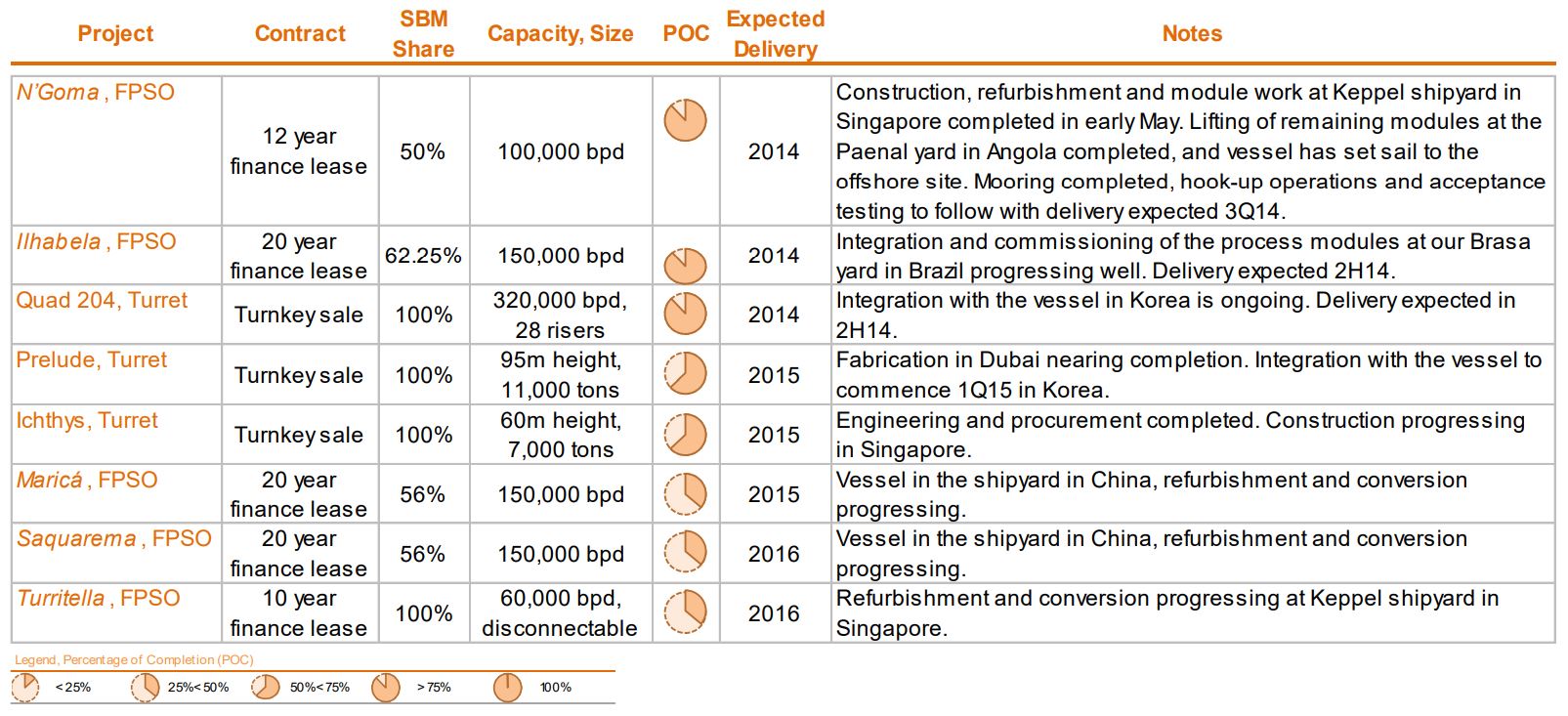

FPSO N’Goma (Angola)

The construction, refurbishment, and module work at Keppel Singapore was completed in early May 2014. A successful lifting campaign at the Paenal yard in Port Amboim, Angola, was completed in July and the vessel set sail to the offshore site where mooring has been completed and hook-up operations and acceptance testing is to follow. The scheduled start of production is in 3Q14 at a design capacity of 100,000 bpd.

FPSO Cidade de Ilhabela (Brazil)

Following completion of refurbishment and conversion at the Chinese yard at the end of 2013, construction continued for the finance leased vessel during the first half of 2014 in Brazil where the process modules were successfully installed at the Brasa yard. The FPSO includes topside facilities able to process 150,000 bpd of production fluids for export, including the substantial volumes of associated gas from the pre-salt field. Start-up of the facility is expected in the second half of 2014.

FPSO Cidade de Maricá and Cidade de Saquarema (Brazil)

Construction is ongoing for the two finance leased vessels. Refurbishment and conversion work progressed during the first half of 2014 at a Chinese yard. The charter contract for both vessels includes an initial period of 20 years with extension options. The two double-hull sister vessels will be moored in approximately 2,300 meters of water depth and possess a storage capacity of 1.6 million barrels each. The topside facilities of each FPSO weigh approximately 22,000 tons, will be able to produce 150,000 bpd of well fluids and have associated gas treatment capacity of 6,000,000 Sm3/d. The water injection capacity of the FPSOs will be 200,000 bpd each.

FPSO Turritella (US Gulf of Mexico)

Construction on the FPSO previously known as Stones continued for the finance leased vessel in the first half of the year, with refurbishment and conversion work continuing at Keppel Singapore. The charter contract includes an initial period of 10 years with extension options up to a total of 20 additional years. In May 2014, the Operations & Maintenance contract was signed with Shell Offshore Inc. When installed at almost 3 kilometers of water depth, the FPSO Turritella will be the deepest offshore production facility of any type in the world. The vessel is a typical Generation 2 design, with a disconnectable internal turret and processing facility capacity of 60,000 barrels of oil per day (bpd) and 15 mmscfd of gas treatment and export.

FPSO Marlim Sul (Brazil)

An extension of six months through the end of 2014 has been agreed to with Petrobras. Negotiations for further extension opportunities beyond 2014 continue.

FPSO Kikeh (Malaysia)

SBM Offshore and its joint venture partner MISC Bhd achieved a key milestone with the start-up of the Siakap North-Petai (SNP) field through a tie-back to the Kikeh FPSO.

The SNP field, a unitized development operated by Murphy Sabah Oil Co.,Ltd (Murphy), is located offshore Malaysia in water depth of approximately 1,300 metres. Murphy announced first oil production from the SNP field on February 27, 2014.

The event is an important milestone for a project that commenced in January 2012 at SBM Offshore’s Kuala Lumpur office and involved the fabrication and offshore lifting of four new modules and approximately 340,000 man-hours of offshore construction and commissioning work done on a live FPSO.

Turret Mooring Systems

The three large, complex turrets for Prelude FLNG, Quad 204 and Ichthys are progressing, in close consultation with the respective clients, on schedule according to their respective stages of project completion. Fabrication work on Prelude FLNG is underway in Dubai, while the integration of the Quad 204 Turret with the vessel continues in South Korea, with expected delivery in the second half of 2014. Engineering and procurement for the Ichthys turret has been completed while construction continues to progress at the yard in Singapore, with expected delivery in the first half of 2015.

Main Projects Overview

HSSE

During the period, SBM Offshore deeply regrets to have to report two fatalities of contractor staff at the relevant yard on construction projects in Singapore. Root cause analysis has been carried out and appropriate measures have been put into effect at contractor facilities.

These fatalities are all the more regrettable, since over the course of the first six months of 2014 the Company achieved an improved safety performance in a range of its business activities, with a Total Recordable Injury Frequency Rate (TRIFR) of 0.26 for the first half of 2014 compared to 0.40 at the end of 2013. The Lost Time Injury Frequency Rate (LTIFR) also improved to 0.06 in the first half of 2014 from 0.15 at the end of 2013.

Compliance

As previously disclosed in various press releases, SBM Offshore voluntarily reported in April 2012 an internal investigation into potentially improper sales practices involving third parties to the relevant authorities, and has since been in dialogue with these authorities.

SBM Offshore is discussing a potential settlement of the issues arising from the investigation. While these discussions are ongoing, it is sufficiently clear that a resolution of the issues will have a financial component, and consequently SBM Offshore has recorded a non-recurring charge of US$240 million in the first half of 2014, reflecting the information currently available to the Company.

Until the matter is concluded, SBM Offshore cannot provide further details regarding a possible resolution of the issues arising from the investigation, and no assurance can be given that a settlement will actually be reached. As always, the Company will inform the market as soon as further information can be provided.

Overheads & Operating Costs

As announced with the Full Year 2013 results on February 6, 2014, SBM Offshore has embarked on a two year programme focused on business improvements, increased fleet maintenance and Research and Development.

The business improvement project Odyssey 24 is aiming to achieve several objectives. It will optimize and consolidate the ways of working of a Company that has quickly grown from a mid-sized centrally managed business to a multi-national, organized in accountable business units. It will improve project management and controls of projects that have grown in size from around US$500 million a few years ago, to close to US$2 billion today. It aims to reduce project costs by at least 5% for each project through improved project, supply chain and materials management, improving both profitability and competitive edge. These financial benefits will accrue to the bottom line increasingly over the next few years. Increased investments in R&D will ensure SBM Offshore stays at the forefront of floating solutions technology, such as complex large turret and swivel systems, thereby opening up new deepwater frontiers for the industry. Finally, a focused increased in offshore maintenance will ensure that the Company is better prepared for long duration lease contracts and contract extensions.

The Company expects incremental annual costs equivalent to 2.5%-3% of Directional¹ revenue in 2014 and 2015. These incremental costs have an impact on the 1H’14 Gross Margin and Overheads, as the investments precede the expected benefits.

Orders

Directional¹ order intake during the first half of 2014 totalled US$1,034 million, driven primarily by the finalization of the FPSO Turritella Operations & Maintenance contract with Shell and the payment of agreed upon variation orders by clients.

Post-Period Events

The Company secured project financing for FPSO Cidade de Maricá totalling US$1.45 billion from a consortium of international banks at a weighted average cost of debt of 5.3%. The financing consists of two tranches, $1.0 billion with a 12 year post-completion maturity and $450 million with 14 year maturity.

Divestment Update

Marketing of the newbuild DSCV SBM Installer continues. The FPSO Falcon and VLCC Alba remain held for sale and the disposal of the last of three Monaco office buildings is nearing completion.

Outlook and Guidance 2014

Management is confidently reiterating 2014 Directional¹ revenue guidance of US$3.3 billion, of which US$2.3 billion is expected in the Turnkey segment and US$1.0 billion in the Lease & Operate segment.

In terms of new FPSOs, SBM Offshore anticipates total industry-wide awards in double digits over the next few years, and the Company is well-positioned to take an appropriate share of the projects which it is targeting. On the timing of individual awards, SBM Offshore is cautious, noting the trend in recent years for tendering processes to lengthen. Nevertheless, it is clear that a substantial body of FPSOs must be commissioned over the next two years for oil & gas companies to maintain production levels.

FINANCIAL REVIEW

IFRS 10, 11 & 12

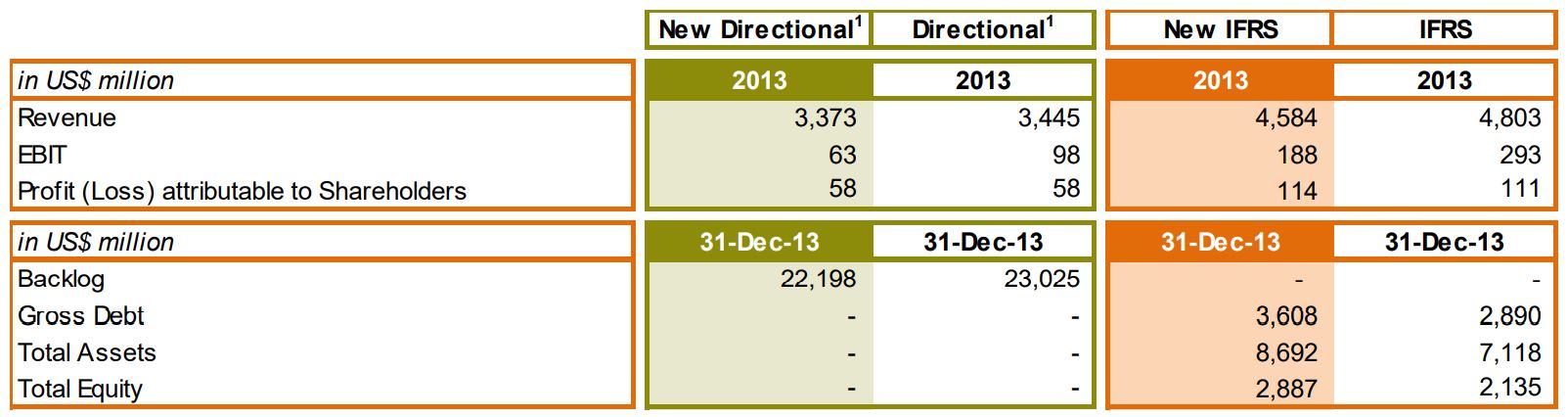

New consolidation standards for joint ventures (JVs) have been introduced as of January 1, 2014 ending proportional consolidation of JVs for SBM Offshore. As disclosed in its 2013 Annual Report, the Company is now required to account for its fully controlled JVs on a fully consolidated basis (mostly impacting all Brazilian FPSOs) and apply equity accounting to the Company’s jointly controlled JVs (mostly Angolan FPSOs). These new standards (IFRS 10, 11 & 12) apply to the income statement, statement of financial position and cash flow statement.

On balance, this implementation has a limited impact on SBM Offshore’s IFRS revenue as the additionally reported partner share in the fully consolidated ventures is offset by the exclusion of revenue in the equity accounted ventures and almost nil to net income attributable to shareholders. However, the Company’s reported total asset value at year-end 2013 has increased significantly by approximately US$1.6 billion, as the now fully consolidated Brazilian assets are younger and represent a larger part of the balance sheet. A similar effect is visible at the gross debt level, increasing from US$2.9 billion to US$3.6 billion. The Company’s 2013 pro-forma financial statements were disclosed in SBM Offshore’s Q1 trading update.

As this change of consolidation rules under IFRS further complicates the understanding of the Company’s performance and as previously announced, Directional¹ reporting will be based on proportional consolidation for all Lease & Operate contracts. Compared to previous Directional¹ reporting, the change is limited to FPSOs Aseng (60% owned)and Capixaba (80% owned) previously fully consolidated and now proportionally consolidated as all other Lease & Operate contracts. This change to Directional¹ reporting led to a limited negative impact of US$35 million and US$5 million in first half 2013 Directional¹ Revenue and EBIT respectively (no impact on Directional¹ net income attributable to shareholders) and restated figures for first half 2013.

Effective January 1, 2014 SBM Offshore’s Directional¹ reporting principles are as follows:

- Directional¹ reporting represents an additional non-GAAP disclosure to IFRS reporting

- Directional¹ reporting assumes all lease contracts are classified as operating leases

- Directional¹ reporting assumes all JVs related to lease contracts are consolidated on a proportional basis

- Directional¹ reporting is limited to restating the consolidated income statement however no restatement of the statement of financial position is made

Directional¹ Performance

In 2013, SBM Offshore decided to extend its reporting with non-IFRS disclosures showing revenue and results (“Directional¹”) more in line with operating cash flows to increase transparency and understanding of the Company’s performance and provide unaudited disclosures of Backlog and Income Statement based on Directional¹ principles.

For more information, a copy of the Directional¹ presentation made to the financial community in June 2013 can be found in the Investor Relations section of the Company website.

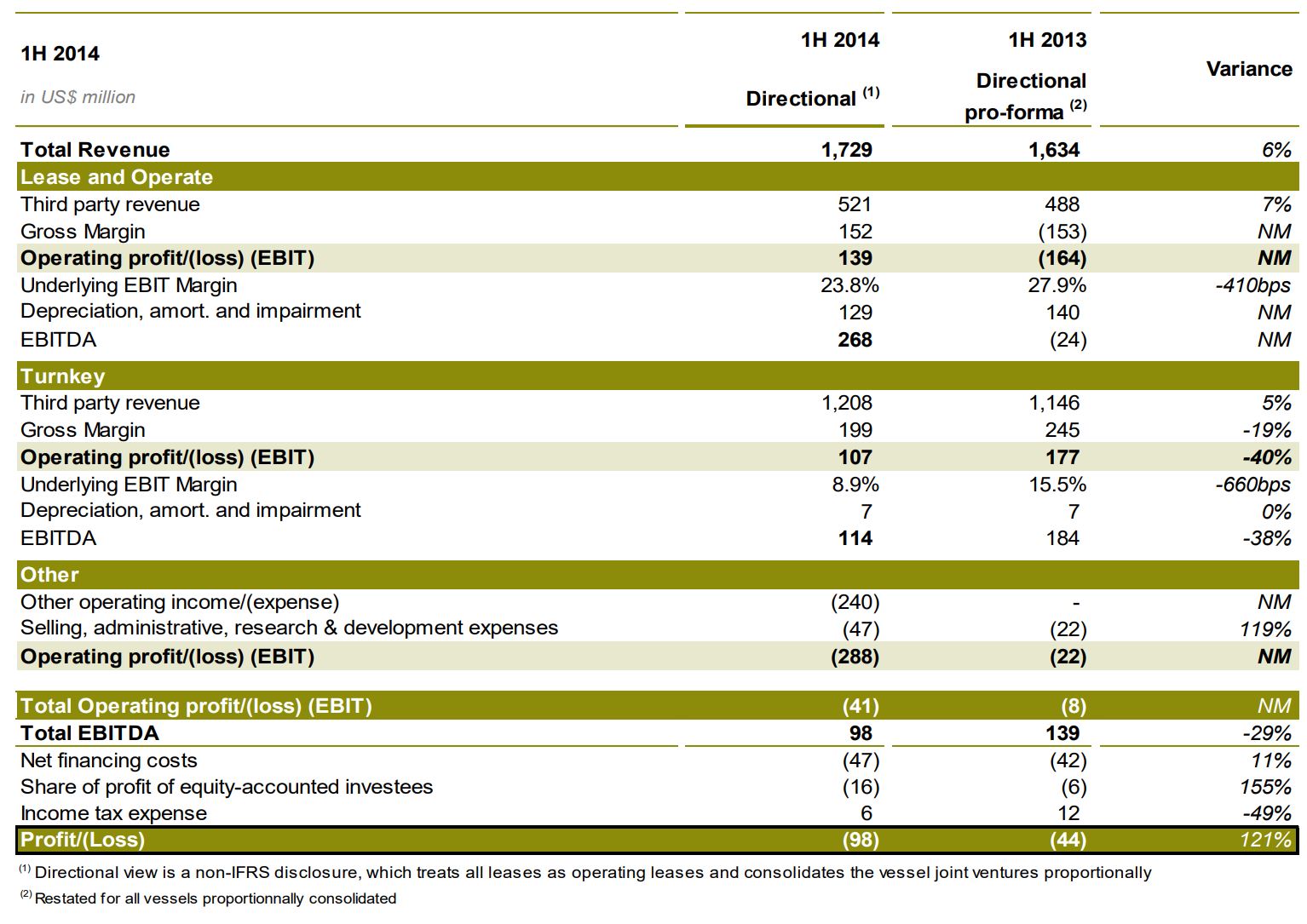

Directional¹ revenue for the first half of 2014 was up by 6% year-over-year to US$1,729 million versus US$1,634 million in the first half of 2013. Directional¹ revenue by segment was as follows:

- Directional¹ Turnkey revenue increased by 5% from the year-ago period reflecting the strong activity on the construction of FPSOs Cidade de Maricá and Saquarema during the first half of 2014.

- Directional¹ Lease and Operate revenue increased by 7% versus the first half of 2013 mainly due to FPSO Cidade de Paraty and theDeep Panuke platform commencing production in June 2013 and August 2013, respectively.

Directional¹ Earnings Before Interest and Taxes (EBIT) for the first half of 2014 represented a loss of US$41 million compared with a loss of US$8 million in the year-ago period. Underlying Directional¹ EBIT excluding the US$270 million charge recorded on Yme and the impairment variances on Deep Panuke along with the US$240 million provision in 2014 for the settlement of the investigation of improper sales practices, decreased by 37% to US$184 million compared to the first half of 2013. This was primarily attributable to:

- Directional¹ Turnkey EBIT decreased by 40% due to the exceptional performance of various projects during the last year period (OSX-2, Fram, Skarv and construction of Cidade de Paraty). Underlying Directional¹ Turnkey EBIT Margin in the first half of 2014 came in at 8.9% compared to 9.6% in the second half of 2013.

- Underlying Directional¹ Lease and Operate EBIT remained stable compared with the year-ago period but includes the impact of increased costs associated with the start-up of the two-year focused fleet maintenance programme. Underlying Directional¹ Lease & Operate EBIT Margin remained stable at 23.8% in the first half of 2014 compared to the second half of 2013.

Directional¹ Overheads expenses reported in the Other segment increased to US$47 million in the first half of 2014 from US$22 million in the year-ago period. The strong year-on-year increase was mainly due to the launch of our two year transformation programme, named Odyssey 24, aiming at laying the foundation to deliver consistent and outstanding performance. In general, Overheads expenses increased also due to additional efforts to maintain our leading technological position, as well as one-off items such as the expenses in relation to our internal investigation and the absence of depreciation during the past period for offices held for sale.

For the first half of 2014, Directional¹ EBITDA decreased to US$98 million. Adjusted for non-recurring events, underlying Directional¹ EBITDA decreased by 19% to US$338 million due to the positive effects of the projects closed-out in 2013 impacting the Turnkey segment.

Directional¹ net financing costs totalled US$47 million in the first half of 2014, up from US$42 million in the year-ago period. The increase was primarily due to the interest costs related to the FPSO Cidade de Paraty project loan as the unit commenced production in June 2013 and mitigated by the decrease of the overall cost of debt during the period.

SBM Offshore recorded a Directional¹ net loss of US$98 million for the first half of 2014 or US$0.47 per share, compared with a US$44 million loss or US$0.22 per share for the first half of 2013. Adjusted for the US$270 million charge recorded on Yme and the impairment variances on Deep Panuke along with the US$240 million provision in 2014 for the settlement of the investigation of potentially improper sales practices, underlying Directional¹ net income decreased by 49% year-on-year to US$127 million or US$0.61 per share, compared to US$252 million or US$1.26 in the first half of 2013 for the reasons stated above.

IFRS Performance

IFRS revenue for the first half of 2014 amounted to US$2,797 million, an increase of 29% compared to US$2,164 million in the year-ago period, mainly as a consequence of significant investments in finance lease contracts.

IFRS EBIT for the first half of 2014 increased significantly from US$74 million to US$201 million despite the US$240 million provision in 2014 for the settlement of the investigation of potentially improper sales practices.

IFRS net income attributable to shareholders came in at US$137 million compared to US$12 million a year ago.

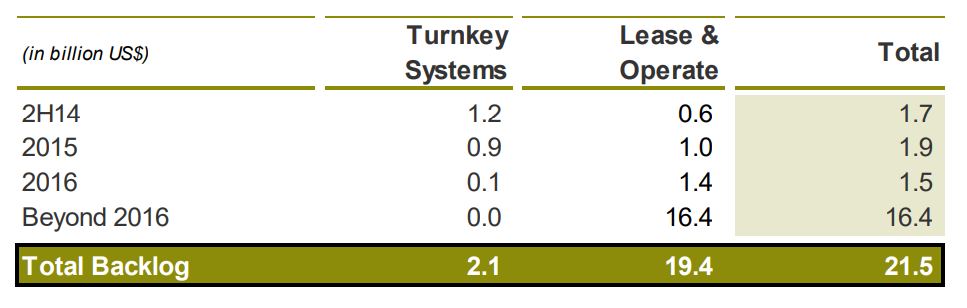

Directional¹ Backlog

Directional¹ Backlog as of June 30, 2014 totalled US$21.5 billion of which approximately US$1.7 billion is expected to be executed over the remainder of 2014. The Backlog at the end of June 2014 includes the Shell Turritella FPSO Operations & Maintenance contract signed in May 2014.

Directional¹ Backlog at the end of June 2014 is as follows:

Statement of Financial Position

The Company has adopted IFRS 10, 11 and 12 in 2014, which had significant consequences for the reported financial statements.

Under new IFRS 10, 11 & 12 consolidation standards for joint ventures (JVs), reported net debt as of December 31, 2013 was restated from US$2,691 million (previous IFRS) to US$3,400 million (new IFRS). As of June 30, 2014 net debt under new IFRS standards increased to US$4,302 million reflecting significant investments in the ongoing Lease and Operate projects under construction for Brazil and Turritella. Cash and cash equivalent balances came in at US$154 million and committed, undrawn, long-term bank facilities stood at US$939 million. The average cost of debt is 4.2% compared to 5.3% at the end of 2013 driven by lower cost of debt on recent bridge loans and projects loans, such as Cidade de Paraty.

Total equity as of June 30, 2014 remained stable at US$2,917 million compared to December 31, 2013. The Company’s net debt to total equity increased from 118% at year-end 2013 to 147% at the end of the first half of 2014. This was primarily due to the strong growth of project debt funding finance lease projects under construction for Brazil as well as the Deep Panuke bridge loan set up in May 2014.

As a result of the significant impacts on the Company’s consolidated statement of financial position relating to the new IFRS 10 and 11 standards instituted in January 2014, the key financial covenants applying to current bank loans had to be recalculated with the view to place the Company and lenders in the same position as they would have been if the change of IFRS standards had not occurred. Restated for the implementation of IFRS 10 and 11, the Company’s solvency ratio stood at 27.5%, firmly within its covenants.

Including cash outflows for finance leases under construction previously reported as investing activities, cash from operating activities was negative US$817 million for the period compared to negative US$420 million during the first half of 2013. Cash outflows in finance leases under construction for the first half of 2014 increased significantly to US$1,370 million compared to US$541 million in the year-ago period taking into consideration the increasing investments in the fully consolidated FPSOs Cidade de Maricá, Saquarema and Turritella. Following the decision to focus the Company’s activities exclusively on FPSOs and FPSO-related products, the disposal process of non-core assets has continued. As of the end of June 2014, the total carrying value of assets presently held for sale amounts to US$177 million.

| Financial Calendar | Date | Year |

| Trading Update Q3 2014 – Press Release | November 13 | 2014 |

| Full-Year 2014 Results – Press Release | February 5 | 2015 |

| Publication of AGM Agenda | March 3 | 2015 |

| Annual General Meeting of Shareholders | April 15 | 2015 |

| Trading Update Q1 2015 – Press Release | May 8 | 2015 |

| Half-Year 2015 Results – Press Release | August 6 | 2015 |

Further financial information is provided in the consolidated interim financial statements included in this press release.²

_______________________________________________________________________

¹ Directional view is a non-IFRS disclosure, which assumes all lease contracts are classified as operating leases and all vessel joint ventures are proportionally consolidated.

² Reflects SBM Offshore’s proportional share in loan facilities.

_______________________________________________________________________

Analyst Presentation & Conference Call

SBM Offshore has scheduled a webcast of its presentation to the financial community and a conference call followed by a Q&A session at 19:30 Central European Summer Time on Wednesday, August 6, 2014.

The presentation will be hosted by Bruno Chabas (CEO), Peter van Rossum (CFO) and Sietze Hepkema (CGCO). Interested parties are invited to listen to the call by dialling +31 20 794 8484 in the Netherlands, +44 207 190 1595 in the UK or +1 480 629 9822 in the US. Conference ID: 4690978. Interested parties may also listen to the presentation via webcast through a link posted on the Investor Relations section of the Company’s website.

A replay of the conference call will be available on Wednesday, August 6, 2014, beginning at 22:00 Central European Summer Time until August 20, 2014. The phone number for the replay is +31 45 799 0028 in the Netherlands and +44 207 959 6720 in the UK using access code 4690978#. The webcast replay will also be available on the Company’s website.

Corporate Profile

SBM Offshore N.V. is a listed holding company that is headquartered in Schiedam. It holds direct and indirect interests in other companies that collectively with SBM Offshore N.V. form the SBM Offshore group (“the Company”).

SBM Offshore provides floating production solutions to the offshore energy industry, over the full product life-cycle. The Company is market leading in leased floating production systems with multiple units currently in operation, and has unrivalled operational experience in this field. The Company’s main activities are the design, supply, installation, operation and the life extension of Floating Production, Storage and Offloading (FPSO) vessels. These are either owned and operated by SBM Offshore and leased to its clients or supplied on a turnkey sale basis.

Group companies employ over 10,983 people worldwide, who are spread over five execution centres, eleven operational shore bases, the joint ventures with several construction yards and the offshore fleet of vessels. Please visit our website at www.sbmoffshore.com.

The companies in which SBM Offshore N.V. directly and indirectly owns investments are separate entities. In this communication “SBM Offshore’is sometimes used for convenience where references are made to SBM Offshore N.V. and its subsidiaries in general, or where no useful purpose is served by identifying the particular company or companies.

The Management Board

Schiedam, August 6, 2014

For further information, please contact:

Investor Relations

Nicolas D. Robert

Head of Investor Relations

| Telephone: | +377 92 05 18 98 |

| Mobile: | +33 (0) 6 40 62 44 79 |

| E-mail: | [emailprotected] |

| Website: | www.sbmoffshore.com |

Media Relations

Anne Guerin-Moens

Group Communications Director

| Telephone: | +377 92 05 30 83 |

| Mobile: | +33 (0) 6 80 86 36 91 |

| E-mail: | [emailprotected] |

| Website: | www.sbmoffshore.com |

Disclaimer

Some of the statements contained in this release that are not historical facts are statements of future expectations and other forward-looking statements based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those in such statements. Such forward-looking statements are subject to various risks and uncertainties, which may cause actual results and performance of the Company’s business to differ materially and adversely from the forward-looking statements. Certain such forward-looking statements can be identified by the use of forward-looking terminology such as “believes”, “may”, “will”, “should”, “would be”, “expects”or “anticipates”or similar expressions, or the negative thereof, or other variations thereof, or comparable terminology, or by discussions of strategy, plans, or intentions. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described in this release as anticipated, bel