Corporate Governance

Articles of Association

Management Board Rules

The division of duties within the Management Board and the procedures of the Management Board are laid down in the enclosed set of rules:

Management Board Remuneration Policy

Supervisory Board Rules

The division of duties within the Supervisory Board and the procedures of the Supervisory Board are laid down in the enclosed set of regulations rules:

Supervisory Board Committee Rules

The Supervisory Board has established three key committees in accordance with the Code. The composition of the committees are set out below, and respective committee rules are attached:

Audit Committee

The Audit Committee’s members are:

D. Dettingmeijer, Chair

I. Arntsen

P.E. Jager

Appointment and Remuneration Committee

The Appointment and Remuneration Committee’s members are:

R.IJ. Baan, Chair selection and appointments

A.S. Castelein, Chair remuneration

P.E. Jager

Technical and Commercial Committee

The Technical and Commercial Committee’s members are:

A.S. Castelein, Chair

L.M. de Andrade

I. Arntsen

Supervisory Board Profile

Profile of the Supervisory Board’s scope and composition

Supervisory Board Remuneration Policy

Supervisory Board Retirement Schedule

The Supervisory Board has drawn up a retirement schedule in order to avoid, as far as possible, a situation in which many Supervisory Board members retire at the same time.

Diversity Policy Management Board and Supervisory Board

Remuneration Reports

Comply or Explain overview Corporate Governance Code

Shareholder Contacts and Dialogue Policy

Stakeholder Engagement Policy

Risk Management

Governance

Risk management is core to the activities conducted by our company. Whether on- or offshore. Within SBM Offshore the Management Board is responsible for the Company’s risk profile and policy, which are designed to realize the Company’s objectives, to assess and manage the Company’s risks and to ensure that internal risk management and control systems are in place. The operation and performance are monitored in an annual assessment by the Management Board and discussed with the Supervisory Board. This monitoring covers all material measures relating to strategic, operational, financial, compliance and reporting risks. Among other considerations, attention is given to observed weaknesses, instances of misconduct and irregularities and indications from whistle blowers.

Management Approach

The Group Risk & Control (GRC), which ultimately reports to the Chief Financial Officer, has a leadership role in proactively facilitating the Management Board and management in its role to manage risks, both from a strategic and an operational perspective. The Group Risk & Control bring the skills to support the business in identifying and managing risks, thereby ensuring the risks are managed within the Risk Appetite in order for the Company to achieve its strategic goals and objectives. As a sounding board, the Risk Assurance Committee (RAC) reviews the significant risks faced by the Company and the relevant control measures. The RAC guards an integrated risk management approach by bringing together the key heads of functions across the second and third line.

Approach to Tax

The payment of taxes is a key element of SBM Offshore’s commitment to contribute to the economic and social development of the countries and communities where we operate. Our tax strategy embodies our Values and is designed to support the delivery of our strategy.

As such SBM Offshore:

- Embraces tax transparency and supports public initiatives for greater transparency and accountability of businesses

- Supports a pro-active stance in terms of compliance and values engagement with tax authorities

- Believes that commercial considerations and substance should drive business structures

- Supports reforms to tax businesses based on where value is created

- Supports initiatives to increase the fairness and effectiveness of tax systems.

SBM Offshore’s tax strategy is based on principles related to the following six themes, which we regard as key to fairness for all and to fulfill our mission, and are further detailed in this document:

- Accountability and governance

- Compliance

- Structure

- Relationships with authorities

- Tax rulings and incentives

- Transparency

Our Tax Strategy

SBM Offshore provides floating production solutions to the offshore energy industry over the full product lifecycle through construction, operation and decommissioning. Our current clients are mainly offshore oil and gas producing companies. We operate in a global context with competitors, clients, suppliers and a workforce based around the world.

In the countries where we operate, we seek to develop and maintain our business on a sustainable basis. We contribute through employment, training, local investment and also through payment of various taxes. These include corporate income tax, withholding tax, sales tax, taxes on wages and salaries, customs duties and other government or indirect taxes where applicable.

The lifecycle of a typical project would include an engineering phase in Europe or Asia and a construction phase in Asia, Africa or South America. For lease and operate projects, after commissioning, SBM Offshore will lease and operate the asset for the benefit of its client for the duration of the lease contract. At the end of the contract, SBM Offshore will decommission the asset at a shipyard usually in a jurisdiction other than the country of operation. In each of these jurisdictions, SBM Offshore is committed to being taxed in accordance with economic substance and value creation.

As part of SBM Offshore’s responsibilities, SBM Offshore endeavours to serve all stakeholders involved in a given project including investors, suppliers, employees and tax authorities.

Accordingly, SBM Offshore aims to pay the proper amount of tax on the profits we make, and in the countries where we create the value that generates those profits. One of our key challenges is to ensure that we pay tax on profits only once and in the right jurisdiction. Achieving this objective requires a careful and consistent application of the tax principles as set out herein.

When the relevant regulations are not clear, the tax authorities in the countries in which we operate may see technical positions in a different light than we do, and this can sometimes lead to disagreements. This could notably happen in the area of transfer pricing. When such controversies arise, we deal with them on the basis of our tax principles.

One of our main challenges is to ensure that we pay tax only once on the profits and that we pay tax in the appropriate jurisdiction.

Tax is aligned with the business and is not a profit center in itself. SBM Offshore’s tax strategy is not only guided by the business objectives of the SBM Offshore Group, but also by its Values, its Tax Principles and the sustainability strategy of the SBM Offshore Group. Just like the tax strategy of the SBM Offshore Group, the Tax Principles are approved by SBM Offshore’s Management Board and provide the guiding principles to exercise this tax strategy.

As a global company, we support initiatives to harmonize tax rules. We support the work of the OECD on international tax reform work on Base Erosion and Profit Shifting (BEPS) and the resulting EU initiatives such as the Anti-Tax Avoidance Directives and the Directive on Administrative Cooperation (DAC 6) on a mandatory disclosure regime. This includes initiatives to increase tax transparency and create a global minimum effective tax rate such as the OECD’s Pillar Two initiative. SBM Offshore is a supporter of the international B-Team Responsible Tax Principles, developed by a group of companies committed to making tax a central part of achieving the UN Sustainable Development Goals. We are also a signatory to Dutch VNO/NCW Tax Governance Code, which is largely based on the B-Team Principles.

Our tax strategy and more generally our approach to tax set out in this document apply to all countries of operations of the SBM Offshore Group including the United Kingdom where it meets the requirements of Finance Act 2016 Schedule 19 Part-2.

Our Tax Principles

Our tax strategy is based on the six following fundamental principles, which we regard as key to ensuring fairness for all and living up to our values.

- Accountability and governance

We have the mechanisms in place to ensure awareness of and adherence to our tax strategy and principles. We provide both relevant training to internal stakeholders and opportunities for employees to raise any concerns confidentially, in line with the SBM Offshore Code of Conduct.

SBM Offshore’s Tax team is part of our finance function, reporting to the Chief Financial Officer. The Group Tax Director has functional accountability for a team of approximately nineteen people with diverse geographical and technical responsibilities. Our staff are suitably qualified and trained professionals with the right level of expertise and understanding, which we constantly seek to improve.

The Management Board and the Audit and Finance Committee of the Supervisory Board receive reports on tax strategy, tax principles and updates on tax regulations and the key tax issues we face. The Audit and Finance Committee receives an annual update on the SBM Offshore Group’s effective tax rate, tax provisions and tax footprint in the various countries in which the Group operates.

The tax team has developed long-term relationships with external tax advisors who provide technical support whenever needed, but we always retain full responsibility for adherence to our tax strategy and principles.

- Compliance

We comply with the tax legislation of the countries in which we operate and pay the proper amount of tax on time, on the profits we earn and in the countries where we create value. We are committed to complying with both the spirit and the letter of the law.

We do not tolerate, encourage or support tax evasion as it is a clear violation of SBM Offshore’s Tax Principles and SBM Offshore Anti-Bribery and Corruption Policy. Doing so may expose the individuals involved to criminal prosecution, as well as exposing SBM Offshore to unnecessary risks. We have a zero-tolerance approach to dealing with such behavior.

Just as the Anti-Bribery and Corruption Policy applies to tax matters, the Group’s Integrity Reporting Policy and the Integrity Reporting Line (SBM Offshore’s whistleblowing mechanism) of the are available for tax-related matters.

Transfer pricing

We pay the proper amount of tax according to where value is created in the ordinary course of business.

Optimizing our business means that we can quickly provide our customers with groundbreaking technical solutions that create value for our clients and our shareholders. As a result, there are many transactions between SBM Offshore Group companies, and the transfer pricing for these transactions must reflect an arm’s length or market price. Our pricing is driven by the activities undertaken and the value created in each part of our business and is in line with the OECD transfer pricing guidelines.

We ensure that our transfer pricing policies are consistently applied and are in line with OECD guidelines and applicable local regulations. In addition, where consistent with the business model and permitted by local regulations, we seek advance pricing agreements with tax authorities. We are committed to paying the proper amount of tax but we also want to avoid competing claims on the same income from different jurisdictions.

- Structure

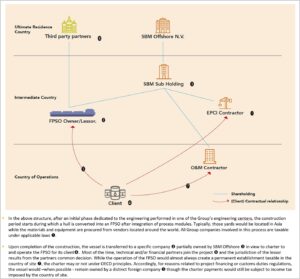

We do not use artificially fragmented structures or contracts that are designed to avoid tax, are not commercially driven, or are not in the spirit of local or international law. A typical FPSO ship structure is as follows:

The jurisdictions of incorporation of entities for associates, joint ventures and joint ownership companies are disclosed in our Annual Report. Jurisdictions other than those of sites and operations may be selected for the incorporation of entities where the absence of a double tax treaty would otherwise result in double taxation of the same profits or where the choice of such jurisdictions is dictated by commercial considerations.

Tax havens

Tax havens can be divided into (1) non-cooperative tax jurisdictions and (2) low-tax jurisdictions.

For non-cooperative tax jurisdictions, we use the EU blacklist of tax havens (i.e. jurisdictions that do not meet the with criteria of transparency, fair tax competition or BEPS implementation) and as of December 31, 2023, we had no operating companies in the SBM Offshore Group located in countries that qualify as non-cooperative tax jurisdictions.

As of December 31, 2023, we had several operating companies in the SBM Offshore Group located in cooperative low-tax jurisdictions. These entities exist for substantive and commercial reasons and can be classified into three categories:

- Fourteen Bermuda companies incorporated between 2002 and 2013, which are either operating companies or holding companies of operating companies:

a. Operating companies are all subject to material withholding taxes in the respective countries of underlying operation. As such the purpose of the Bermuda companies is not to divert taxable income from the countries of underlying operations. Rather, their purpose is to avoid a double taxation in the case of operations in jurisdictions without double tax treaties;

b. The Bermuda holding companies are not intended to generate profits (other than those arising from timing differences in the recognition of provisions or from their participation, which would be tax exempt under the EU participation exemption rules) and therefore do not affect the tax liability of the SBM Offshore Group. Furthermore, the fourteen Bermuda companies of the SBM Offshore Group are all joint ventures and the choice of jurisdiction was therefore a commercial decision made by several partners and lenders. Accordingly, changing these structures is not something SBM Offshore can do on its own.

- Three Cayman Islands companies:

a. Two of which are operating companies established in 2009 and only partly owned by SBM Offshore. As with the Bermuda entities, the choice of jurisdiction was a commercial decision made by several partners and lenders and changing those structures is not something SBM Offshore can do on its own;

b. The third is a group financing company established in 1992. Its main role is limited to corporate financing of old group companies operating in West Africa. No new financing has been done by this company in the last eight years, so it can and will be phased out as the underlying financings have reached their tenor.

- Dormant companies domiciled in various low-tax jurisdictions and scheduled for deregistration.

SBM Offshore has not established entities in low-tax jurisdictions since 2013 and refrains from using such jurisdictions for new projects unless the choice of such jurisdiction is dictated by substantive and commercial reasons.

- Relationships with authorities

Where possible, we seek to develop strong cooperative relationships with tax authorities, based on mutual respect, transparency and trust. We also support, where requested, initiatives that contribute to the development of the capability of tax authorities and tax systems.

We encourage open and transparent dialogue with tax authorities, and dialogue in advance of entering into transactions and filing tax returns when there is an uncertainty about how the tax rules apply to our business.

For example, in the Netherlands, Monaco and Switzerland, we engage with the tax authorities through regular meetings, calls and correspondence whenever a material topic needs to be discussed. This allows us to identify potential issues, explore options to resolve any misunderstandings or disagreements, and increase the certainty of tax positions. The same approach is taken where possible in all jurisdictions including with HMRC in the United Kingdom.

We also welcome the opportunity to work with other stakeholders taking into account their interests. Through engagement with non-profit initiatives (such as the B Team Responsible Tax Working Group) and business organizations (such as the Swiss Shipowners Association and the Dutch VNO-NCW), we remain informed about the views and concerns of external stakeholders and provide policymakers with our technical thinking and relevant business insights.

- Tax rulings and incentives

We seek rulings from tax authorities only to confirm an applicable treatment and we do so based on full disclosure of all the relevant facts and circumstances.

Tax incentives are government policies that are designed to influence business decisions by incentivizing or promoting a particular economic activity, by providing a more favorable tax treatment for certain activities or sectors compared to that which generally applies. We seek to take advantage of tax incentives only when they are aligned with our business and operating objectives and are based on economic substance.

If the facts and circumstances underlying a particular tax ruling or incentive were to materially change, we would engage in discussions with the authorities in the relevant jurisdictions to reflect the change in circumstances using publicly available transition mechanisms.

- Transparency

We are transparent about our approach to tax. We provide regular information about our approach to tax and the total taxes paid.

The SBM Offshore Group is required to submit a detailed report in accordance with BEPS Action 13, as is now implemented in Dutch tax law. The information contained in the country-by-country reporting (CbCR) is prepared in accordance with OECD requirements and submitted to the Dutch tax authorities.

Tax Risk Framework

To succeed in today’s rapidly changing world of complex international tax regulations and reporting requirements, we must manage risk. To achieve this, we embed risk management into important decisions and day-to-day operations, and channel it proactively and positively, in line with our tax principles. We have a low appetite for taking tax risk and therefore proactively seek to identify, assess, manage and monitor this risk to ensure it remains in line with SBM Offshore risk appetite.

Risk is managed through our Tax Risk Framework. This sets out the key tax risks and the mitigating actions that we take to manage and monitor these risks.

Risks are monitored on a quarterly basis by the Tax team through a review of all our tax exposures and provisions. The Tax Risk Framework also includes a semi-annual review of compliance with our Tax Principles by the Management Board and the Audit and Finance Committee of the Supervisory Board. If the results of the review identify such a need, this would lead to an update of the Tax Strategy and of the underlying Tax Principles

As part of this review, a tax in-control statement is issued by the Group Tax Director, validated by the Management Board and presented to the Audit and Finance Committee of the Supervisory Board. Furthermore, the Group’s Internal Control department performs a regular formal review of the Internal Controls over Financial Reporting, including tax controls.

SBM Offshore is subject to taxation in multiple jurisdictions. Tax legislation is often complex and constantly evolving. Significant judgement is required, and tax positions are sometimes subject to interpretation including by local tax authorities. Our risk management policy sets out the steps we take to mitigate our tax exposure and to ensure we properly assess and report our uncertain tax positions

- As part of our tax policy, all assessments, tax audits and notifications received from local tax authorities are centralized at SBM Offshore Group level.

- Where necessary, SBM Offshore engages with local tax advisors to advise on the likely position of the tax authorities on the treatment of an uncertain tax position.

- SBM Offshore considers any changes in tax legislation and uses knowledge gained from past cases to make an estimate of whether or not to provide for any tax payable.

- SBM Offshore takes into account any settlements of disputes, case law and discussions between peer companies and the tax authorities on similar cases regarding uncertain tax treatment.

SBM Offshore determines the likelihood that a tax authority will have a different interpretation of a tax position. This risk is assessed and reported on a regular basis to Group Control, the Management Board and the Audit and Finance Committee of the Supervisory Board in accordance with approved Group policies.

We continue to improve the quality of our Tax Risk Framework through the use of technology, including tools to consolidate, share and accurately report data. We have developed and implemented software to ensure the quality of our tax reporting.

Technology has a major impact on the tax function. By using it to increase the quality and quantity of data, SBM Offshore is in a position to better assess the application of its Tax Principles.

Tax Reporting

The consolidated financial statements of the SBM Offshore Group are prepared in accordance with International Financial Reporting Standards (IFRS) as well as Directional reporting, which is presented in the Financial Statements under Operating segments and Directional (“Directional”) reporting. Directional reporting represents a pro forma accounting policy that essentially assumes that all lease contracts are classified as operating leases and that all vessel investments are proportionally consolidated to more closely align with the cash generation of the company. For more detail on the main principles of Directional reporting, please refer to section 4.3.2 of the 2023 Annual Report.

SBM Offshore’s operations generate significant tax revenues for the governments in the countries in which we operate. In addition to corporate income taxes, we pay and collect numerous other taxes. These include employee taxes, sales taxes, customs duties and local transaction taxes. In 2023, we made global tax payments of US$ 374 million (2022: US$297) as disclosed below.

See also our Tax Contribution per Jurisdiction.

Total tax paid and/or payable by type in 2023 (IFRS)

| Tax Type | Tax paid and/or payable in 2023 (US$ million) |

| Corporate tax (1) (2) | 130 |

| Sales taxes -output transactions – | 11 |

| Employment taxes | 197 |

| Other taxes | 36 |

| Total tax borne | 374 |

Notes:

- Corporate income tax includes withholding tax.

- The amount stood at US$ 87 million for 2022, reflecting notably a material increase in corporate tax paid in Guyana in 2023.

There are a number of reasons why cash payments for corporate income tax in a particular year may differ from the corporate income tax expense reported in the financial statements, including deferred taxes and provisions for uncertain positions.

- Deferred taxes: The Group’s tax expense includes deferred taxes resulting from timing differences between the recognition of gains and losses in the financial statements and their recognition for tax purpose.

- Provisions for uncertain tax positions: We are subject to taxation in the countries in which we operate. Despite our cooperation with the tax authorities, it is sometimes uncertain whether our position on a given tax matter will be accepted by the competent tax authority. As a result, we may be required to record a provision for potential tax payments in future years, which is generally estimated using the single-most-likely-amount method.

SBM Offshore Effective Tax Rate in 2023

SBM Offshore reports its financial results based both on the Directional reporting method (as defined and for the reasons explained above under Tax Reporting.) and on IFRS standard.

Under Directional reporting, the effective corporate income tax rate (ETR) for the year 2023 is 5.4%. This is our worldwide corporate income tax expense in the SBM Offshore 2023 consolidated income statement under Directional reporting of US$ 29.5 million (2022: US$ 87.8 million), expressed as a percentage of the Group’s worldwide income before tax.

Under IFRS, our ETR in 2023 was -4.4% (2022: 16.1%). This is our worldwide corporate income tax expense in the SBM Offshore 2023 consolidated income statement under IFRS of US$ -25.2 million (2022: US$ 104.2 million), shown as a percentage of the worldwide Group profit before tax. The difference between IFRS and Directional is primarily due to the fact that in so-called uncontrolled joint ventures i. IFRS does not separately report taxes actually paid, while ii. the income tax charge is recognized in proportion of SBM’s shares in Directional.

If adjusted to exclude the largest extraordinary items such as uncertain tax and deferred tax positions, the ETR for 2023 would be approximately 52.6% (Directional) and 26.5% (IFRS).

SBM Offshore’s future tax expense and ETR may be affected by several factors. First and foremost, SBM Offshore’s ETR is heavily influenced by the evolution of the statutory tax rate of the jurisdictions where the FPSO fleet is operated and the relative weight of these jurisdictions in the fleet portfolio. This can change over time as new assets are brought into service and other assets are decommissioned. The ETR is also affected by changes in tax laws and their interpretation, yet-to-be-determined EU tax reform proposals, the ongoing OECD international tax reform work, including Pillar Two, as well as the impact of acquisitions, divestments and any restructuring of our businesses.

SBM Offshore will be affected by Pillar Two, effective as of 2024 as it will significantly increase compliance requirements and may result in an additional tax burden. We are preparing for the implementation of Pillar 2 by enhancing our existing tax infrastructure in order to ensure an efficient and accurate process, calculate the top-up tax liability (if any), and enable timely filing.